Page 16 - DEBKVOL-1

P. 16

1.6 Double Entry Book Keeping—CBSE XII

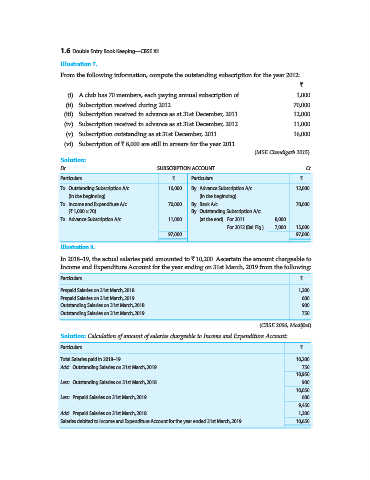

Illustration 7.

From the following information, compute the outstanding subscription for the year 2012:

`

(i) A club has 70 members, each paying annual subscription of 1,000

(ii) Subscription received during 2012 70,000

(iii) Subscription received in advance as at 31st December, 2011 12,000

(iv) Subscription received in advance as at 31st December, 2012 11,000

(v) Subscription outstanding as at 31st December, 2011 16,000

(vi) Subscription of ` 8,000 are still in arrears for the year 2011

(MSE Chandigarh 2015)

Solution:

Dr. SUBSCRIPTION ACCOUNT Cr.

Particulars ` Particulars `

To Outstanding Subscription A/c 16,000 By Advance Subscription A/c 12,000

(in the beginning) (in the beginning)

To Income and Expenditure A/c 70,000 By Bank A/c 70,000

(` 1,000 × 70) By Outstanding Subscription A/c:

To Advance Subscription A/c 11,000 (at the end) For 2011 8,000

For 2012 (Bal. Fig.) 7,000 15,000

97,000 97,000

Illustration 8.

In 2018–19, the actual salaries paid amounted to ` 10,200. Ascertain the amount chargeable to

Income and Expenditure Account for the year ending on 31st March, 2019 from the following:

Particulars `

Prepaid Salaries on 31st March, 2018 1,200

Prepaid Salaries on 31st March, 2019 600

Outstanding Salaries on 31st March, 2018 900

Outstanding Salaries on 31st March, 2019 750

(CBSE 2006, Modified)

Solution: Calculation of amount of salaries chargeable to Income and Expenditure Account:

Particulars `

Total Salaries paid in 2018–19 10,200

Add: Outstanding Salaries on 31st March, 2019 750

10,950

Less: Outstanding Salaries on 31st March, 2018 900

10,050

Less: Prepaid Salaries on 31st March, 2019 600

9,450

Add: Prepaid Salaries on 31st March, 2018 1,200

Salaries debited to Income and Expenditure Account for the year ended 31st March, 2019 10,650