Page 18 - DEBKVOL-1

P. 18

1.8 Double Entry Book Keeping—CBSE XII

Illustration 10.

From the following information, prepare Income and Expenditure Account of the Club for the

year ended 31st March, 2013 and ascertain the Capital Fund on 31st March, 2012:

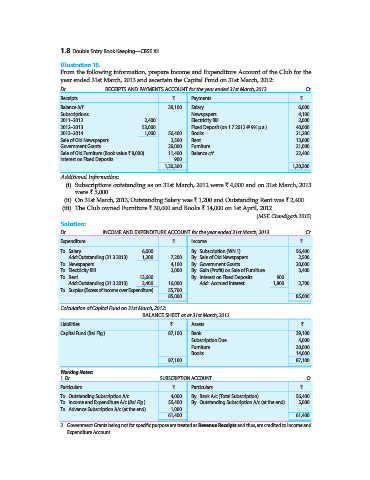

Dr. RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2013 Cr.

Receipts ` Payments `

Balance b/f 39,100 Salary 6,000

Subscriptions: Newspapers 4,100

2011–2012 2,400 Electricity Bill 2,000

2012–2013 53,000 Fixed Deposit (on 1.7.2012 @ 9% p.a.) 40,000

2013–2014 1,000 56,400 Books 21,200

Sale of Old Newspapers 2,500 Rent 13,600

Government Grants 20,000 Furniture 21,000

Sale of Old Furniture (Book value ` 8,000) 11,400 Balance c/f 22,400

Interest on Fixed Deposits 900

1,30,300 1,30,300

Additional Information:

(i) Subscriptions outstanding as on 31st March, 2012 were ` 4,000 and on 31st March, 2013

were ` 5,000.

(ii) On 31st March, 2013, Outstanding Salary was ` 1,200 and Outstanding Rent was ` 2,400.

(iii) The Club owned Furniture ` 30,000 and Books ` 14,000 on 1st April, 2012.

(MSE Chandigarh 2015)

Solution:

Dr. INCOME AND EXPENDITURE ACCOUNT for the year ended 31st March, 2013 Cr.

Expenditure ` Income `

To Salary 6,000 By Subscription (WN 1) 56,400

Add: Outstanding (31.3.2013) 1,200 7,200 By Sale of Old Newspapers 2,500

To Newspapers 4,100 By Government Grants 20,000

To Electricity Bill 2,000 By Gain (Profit) on Sale of Furniture 3,400

To Rent 13,600 By Interest on Fixed Deposits 900

Add: Outstanding (31.3.2013) 2,400 16,000 Add: Accrued Interest 1,800 2,700

To Surplus (Excess of Income over Expenditure) 55,700

85,000 85,000

Calculation of Capital Fund on 31st March, 2012:

BALANCE SHEET as at 31st March, 2012

Liabilities ` Assets `

Capital Fund (Bal. Fig.) 87,100 Bank 39,100

Subscription Due 4,000

Furniture 30,000

Books 14,000

87,100 87,100

Working Notes:

1. Dr. SUBSCRIPTION ACCOUNT Cr.

Particulars ` Particulars `

To Outstanding Subscription A/c 4,000 By Bank A/c (Total Subscription) 56,400

To Income and Expenditure A/c (Bal. Fig.) 56,400 By Outstanding Subscription A/c (at the end) 5,000

To Advance Subscription A/c (at the end) 1,000

61,400 61,400

2. Government Grants being not for specific purpose are treated as Revenue Receipts and thus, are credited to Income and

Expenditure Account.