Page 141 - DEBKVOL-1

P. 141

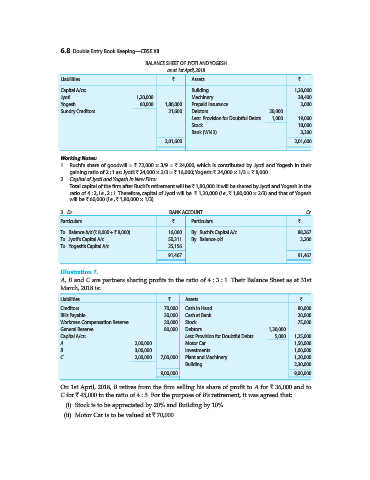

6.8 Double Entry Book Keeping—CBSE XII

BALANCE SHEET OF JYOTI AND YOGESH

as at 1st April, 2018

Liabilities ` Assets `

Capital A/cs: Building 1,20,000

Jyoti 1,20,000 Machinery 38,400

Yogesh 60,000 1,80,000 Prepaid Insurance 3,000

Sundry Creditors 21,600 Debtors 20,000

Less: Provision for Doubtful Debts 1,000 19,000

Stock 18,000

Bank (WN 3) 3,200

2,01,600 2,01,600

Working Notes:

1. Ruchi’s share of goodwill = ` 72,000 × 3/9 = ` 24,000, which is contributed by Jyoti and Yogesh in their

gaining ratio of 2 : 1 as: Jyoti: ` 24,000 × 2/3 = ` 16,000; Yogesh: ` 24,000 × 1/3 = ` 8,000.

2. Capital of Jyoti and Yogesh in New Firm:

Total capital of the firm after Ruchi’s retirement will be ` 1,80,000. It will be shared by Jyoti and Yogesh in the

ratio of 4 : 2, i.e., 2 : 1. Therefore, capital of Jyoti will be ` 1,20,000 (i.e., ` 1,80,000 × 2/3) and that of Yogesh

will be ` 60,000 (i.e., ` 1,80,000 × 1/3).

3. Dr. BANK ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d (` 8,000 + ` 8,000) 16,000 By Ruchi’s Capital A/c 88,267

To Jyoti’s Capital A/c 50,311 By Balance c/d 3,200

To Yogesh’s Capital A/c 25,156

91,467 91,467

Illustration 7.

A, B and C are partners sharing profits in the ratio of 4 : 3 : 1. Their Balance Sheet as at 31st

March, 2018 is:

Liabilities ` Assets `

Creditors 70,000 Cash in Hand 80,000

Bills Payable 30,000 Cash at Bank 20,000

Workmen Compensation Reserve 20,000 Stock 75,000

General Reserve 80,000 Debtors 1,30,000

Capital A/cs: Less: Provision for Doubtful Debts 5,000 1,25,000

A 2,00,000 Motor Car 1,50,000

B 3,00,000 Investments 1,00,000

C 2,00,000 7,00,000 Plant and Machinery 1,20,000

Building 2,30,000

9,00,000 9,00,000

On 1st April, 2018, B retires from the firm selling his share of profit to A for ` 36,000 and to

C for ` 45,000 in the ratio of 4 : 5. For the purpose of B’s retirement, it was agreed that:

(i) Stock is to be appreciated by 20% and Building by 10%.

(ii) Motor Car is to be valued at ` 70,000.