Page 146 - DEBKVOL-1

P. 146

Chapter 6 Retirement of a Partner 6.13

.

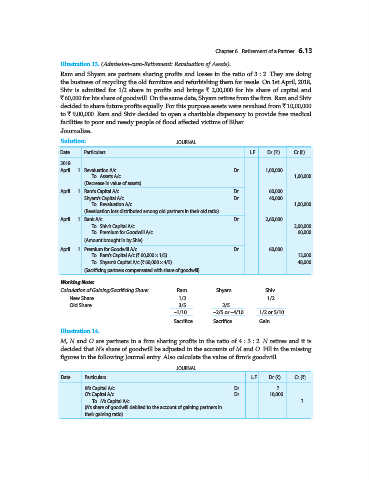

Illustration 13. (Admission-cum-Retirement: Revaluation of Assets).

Ram and Shyam are partners sharing profits and losses in the ratio of 3 : 2. They are doing

the business of recycling the old furniture and refurbishing them for resale. On 1st April, 2018,

Shiv is admitted for 1/2 share in profits and brings ` 2,00,000 for his share of capital and

` 60,000 for his share of goodwill. On the same date, Shyam retires from the firm. Ram and Shiv

decided to share future profits equally. For this purpose assets were revalued from ` 10,00,000

to ` 9,00,000. Ram and Shiv decided to open a charitable dispensary to provide free medical

facilities to poor and needy people of flood affected victims of Bihar.

Journalise.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2018

April 1 Revaluation A/c ...Dr. 1,00,000

To Assets A/c 1,00,000

(Decrease in value of assets)

April 1 Ram’s Capital A/c ...Dr. 60,000

Shyam’s Capital A/c ...Dr. 40,000

To Revaluation A/c 1,00,000

(Revaluation loss distributed among old partners in their old ratio)

April 1 Bank A/c ...Dr. 2,60,000

To Shiv’s Capital A/c 2,00,000

To Premium for Goodwill A/c 60,000

(Amount brought in by Shiv)

April 1 Premium for Goodwill A/c ...Dr. 60,000

To Ram’s Capital A/c (` 60,000 × 1/5) 12,000

To Shyam’s Capital A/c (` 60,000 × 4/5) 48,000

(Sacrificing partners compensated with share of goodwill)

Working Note:

Calculation of Gaining/Sacrificing Share: Ram Shyam Shiv

New Share 1/2 ... 1/2

Old Share 3/5 2/5 ...

–1/10 –2/5 or –4/10 1/2 or 5/10

Sacrifice Sacrifice Gain

Illustration 14.

M, N and O are partners in a firm sharing profits in the ratio of 4 : 3 : 2. N retires and it is

decided that N’s share of goodwill be adjusted in the accounts of M and O. Fill in the missing

figures in the following Journal entry. Also calculate the value of firm’s goodwill.

JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

M’s Capital A/c ...Dr. ?

O’s Capital A/c ...Dr. 10,000

To N’s Capital A/c ?

(N’s share of goodwill debited to the account of gaining partners in

their gaining ratio)