Page 145 - DEBKVOL-1

P. 145

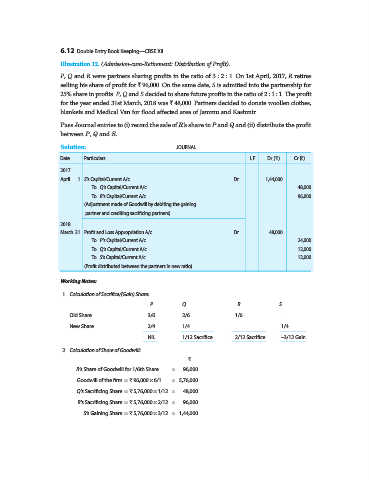

6.12 Double Entry Book Keeping—CBSE XII

Illustration 12. (Admission-cum-Retirement: Distribution of Profit).

P, Q and R were partners sharing profits in the ratio of 3 : 2 : 1. On 1st April, 2017, R retires

selling his share of profit for ` 96,000. On the same date, S is admitted into the partnership for

25% share in profits. P, Q and S decided to share future profits in the ratio of 2 : 1 : 1. The profit

for the year ended 31st March, 2018 was ` 48,000. Partners decided to donate woollen clothes,

blankets and Medical Van for flood affected area of Jammu and Kashmir.

Pass Journal entries to (i) record the sale of R’s share to P and Q and (ii) distribute the profit

between P, Q and S.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2017

April 1 S’s Capital/Current A/c ...Dr. 1,44,000

To Q’s Capital/Current A/c 48,000

To R’s Capital/Current A/c 96,000

(Adjustment made of Goodwill by debiting the gaining

partner and crediting sacrificing partners)

2018

March 31 Profit and Loss Appropriation A/c ...Dr. 48,000

To P’s Capital/Current A/c 24,000

To Q’s Capital/Current A/c 12,000

To S’s Capital/Current A/c 12,000

(Profit distributed between the partners in new ratio)

Working Notes:

1. Calculation of Sacrifice/(Gain) Share:

P Q R S

Old Share 3/6 2/6 1/6 ...

New Share 2/4 1/4 ... 1/4

NIL 1/12 Sacrifice 2/12 Sacrifice –3/12 Gain

2. Calculation of Share of Goodwill:

`

R’s Share of Goodwill for 1/6th Share = 96,000

Goodwill of the firm = ` 96,000 × 6/1 = 5,76,000

Q’s Sacrificing Share = ` 5,76,000 × 1/12 = 48,000

R’s Sacrificing Share = ` 5,76,000 × 2/12 = 96,000

S’s Gaining Share = ` 5,76,000 × 3/12 = 1,44,000