Page 154 - DEBKVOL-1

P. 154

Chapter 6 Retirement of a Partner 6.21

.

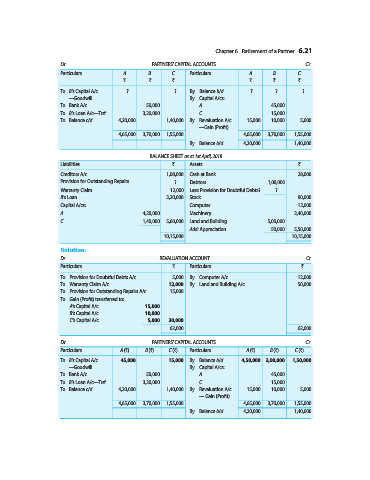

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars A B C Particulars A B C

` ` ` ` ` `

To B’s Capital A/c ? ? By Balance b/d ? ? ?

—Goodwill By Capital A/cs:

To Bank A/c 50,000 A 45,000

To B’s Loan A/c—Trsf. 3,20,000 C 15,000

To Balance c/d 4,20,000 1,40,000 By Revaluation A/c 15,000 10,000 5,000

—Gain (Profit)

4,65,000 3,70,000 1,55,000 4,65,000 3,70,000 1,55,000

By Balance b/d 4,20,000 1,40,000

BALANCE SHEET as at 1st April, 2018

Liabilities ` Assets `

Creditors A/c 1,08,000 Cash at Bank 28,000

Provision for Outstanding Repairs ? Debtors 1,00,000

Warranty Claim 12,000 Less: Provision for Doubtful Debts ? ?

B’s Loan 3,20,000 Stock 90,000

Capital A/cs: Computer 12,000

A 4,20,000 Machinery 2,40,000

C 1,40,000 5,60,000 Land and Building 5,00,000

Add: Appreciation 50,000 5,50,000

10,15,000 10,15,000

Solution:

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Provision for Doubtful Debts A/c 5,000 By Computer A/c 12,000

To Warranty Claim A/c 12,000 By Land and Building A/c 50,000

To Provision for Outstanding Repairs A/c 15,000

To Gain (Profit) transferred to:

A’s Capital A/c 15,000

B’s Capital A/c 10,000

C’s Capital A/c 5,000 30,000

62,000 62,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars A (`) B (`) C (`) Particulars A (`) B (`) C (`)

To B’s Capital A/c 45,000 15,000 By Balance b/d 4,50,000 3,00,000 1,50,000

—Goodwill By Capital A/cs:

To Bank A/c 50,000 A 45,000

To B’s Loan A/c—Trsf. 3,20,000 C 15,000

To Balance c/d 4,20,000 1,40,000 By Revaluation A/c 15,000 10,000 5,000

— Gain (Profit)

4,65,000 3,70,000 1,55,000 4,65,000 3,70,000 1,55,000

By Balance b/d 4,20,000 1,40,000