Page 155 - DEBKVOL-1

P. 155

6.22 Double Entry Book Keeping—CBSE XII

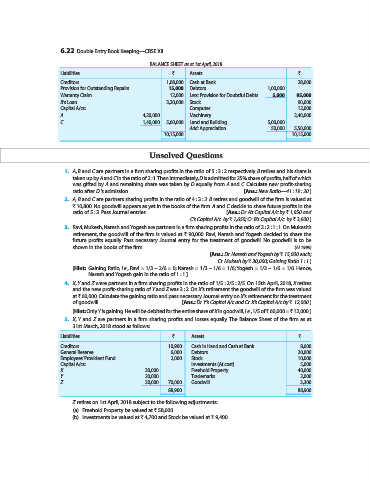

BALANCE SHEET as at 1st April, 2018

Liabilities ` Assets `

Creditors 1,08,000 Cash at Bank 28,000

Provision for Outstanding Repairs 15,000 Debtors 1,00,000

Warranty Claim 12,000 Less: Provision for Doubtful Debts 5,000 95,000

B’s Loan 3,20,000 Stock 90,000

Capital A/cs: Computer 12,000

A 4,20,000 Machinery 2,40,000

C 1,40,000 5,60,000 Land and Building 5,00,000

Add: Appreciation 50,000 5,50,000

10,15,000 10,15,000

Unsolved Questions

1. A, B and C are partners in a firm sharing profits in the ratio of 5 : 3 : 2 respectively. B retires and his share is

taken up by A and C in the ratio of 2 : 1. Then immediately, D is admitted for 25% share of profits, half of which

was gifted by A and remaining share was taken by D equally from A and C. Calculate new profit-sharing

ratio after D ’s admission. [Ans.: New Ratio—41 : 19 : 20.]

2. A, B and C are partners sharing profits in the ratio of 4 : 3 : 2. B retires and goodwill of the firm is valued at

` 10,800. No goodwill appears as yet in the books of the firm. A and C decide to share future profits in the

ratio of 5 : 3. Pass Journal entries. [Ans.: Dr. A’s Capital A/c by ` 1,950 and

C’s Capital A/c by ` 1,650; Cr. B’s Capital A/c by ` 3,600.]

3. Ravi, Mukesh, Naresh and Yogesh are partners in a firm sharing profits in the ratio of 2 : 2 : 1 : 1. On Mukesh’s

retirement, the goodwill of the firm is valued at ` 90,000. Ravi, Naresh and Yogesh decided to share the

future profits equally. Pass necessary Journal entry for the treatment of goodwill. No goodwill is to be

shown in the books of the firm. (AI 1999)

[Ans.: Dr. Naresh and Yogesh by ` 15,000 each;

Cr. Mukesh by ` 30,000; Gaining Ratio 1 : 1.]

[Hint: Gaining Ratio, i.e., Ravi = 1/3 – 2/6 = 0; Naresh = 1/3 – 1/6 = 1/6; Yogesh = 1/3 – 1/6 = 1/6. Hence,

Naresh and Yogesh gain in the ratio of 1 : 1.]

4. X, Y and Z were partners in a firm sharing profits in the ratio of 1/5 : 2/5 : 2/5. On 15th April, 2018, X retires

and the new profit-sharing ratio of Y and Z was 3 : 2. On X’s retirement the goodwill of the firm was valued

at ` 60,000. Calculate the gaining ratio and pass necessary Journal entry on X’s retirement for the treatment

of goodwill. [Ans.: Dr. Y’s Capital A/c and Cr. X’s Capital A/c by ` 12,000.]

[Hint: Only Y is gaining. He will be debited for the entire share of X in goodwill, i.e., 1/5 of ` 60,000 = ` 12,000.]

5. X, Y and Z are partners in a firm sharing profits and losses equally. The Balance Sheet of the firm as at

31st March, 2018 stood as follows:

Liabilities ` Assets `

Creditors 10,900 Cash in Hand and Cash at Bank 8,600

General Reserve 6,000 Debtors 20,000

Employees’ Provident Fund 2,000 Stock 10,000

Capital A/cs: Investments (At cost) 5,000

X 30,000 Freehold Property 40,000

Y 20,000 Trademarks 2,000

Z 20,000 70,000 Goodwill 3,300

88,900 88,900

Z retires on 1st April, 2018 subject to the following adjustments:

(a) Freehold Property be valued at ` 58,000.

(b) Investments be valued at ` 4,700 and Stock be valued at ` 9,400.