Page 160 - DEBKVOL-1

P. 160

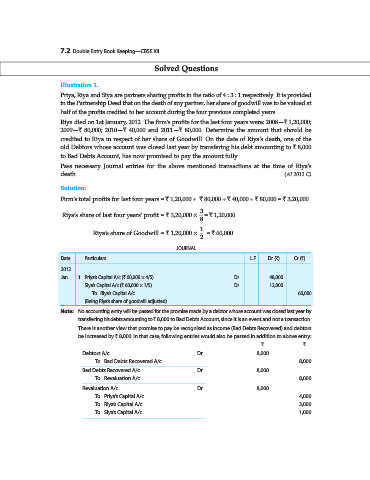

7.2 Double Entry Book Keeping—CBSE XII

Solved Questions

Illustration 1.

Priya, Riya and Siya are partners sharing profits in the ratio of 4 : 3 : 1 respectively. It is provided

in the Partnership Deed that on the death of any partner, her share of goodwill was to be valued at

half of the profits credited to her account during the four previous completed years.

Riya died on 1st January, 2012. The firm’s profits for the last four years were: 2008—` 1,20,000;

2009—` 80,000; 2010—` 40,000 and 2011—` 80,000. Determine the amount that should be

credited to Riya in respect of her share of Goodwill. On the date of Riya’s death, one of the

old Debtors whose account was closed last year by transfering his debt amounting to ` 8,000

to Bad Debts Account, has now promised to pay the amount fully.

Pass necessary Journal entries for the above mentioned transactions at the time of Riya’s

death. (AI 2012 C)

Solution:

Firm’s total profits for last four years = ` 1,20,000 + ` 80,000 + ` 40,000 + ` 80,000 = ` 3,20,000

3

Riya’s share of last four years’ profit = ` 3,20,000 × = ` 1,20,000

8

1

Riya’s share of Goodwill = ` 1,20,000 × = ` 60,000.

2

JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2012

Jan. 1 Priya’s Capital A/c (` 60,000 × 4/5) ...Dr. 48,000

Siya’s Capital A/c (` 60,000 × 1/5) ...Dr. 12,000

To Riya’s Capital A/c 60,000

(Being Riya’s share of goodwill adjusted)

Note: No accounting entry will be passed for the promise made by a debtor whose account was closed last year by

transferring his debts amounting to ` 8,000 to Bad Debts Account, since it is an event and not a transaction.

There is another view that promise to pay be recognised as income (Bad Debts Recovered) and debtors

be increased by ` 8,000. In that case, following entries would also be passed in addition to above entry:

` `

Debtors A/c ...Dr. 8,000

To Bad Debts Recovered A/c 8,000

Bad Debts Recovered A/c ...Dr. 8,000

To Revaluation A/c 8,000

Revaluation A/c ...Dr. 8,000

To Priya’s Capital A/c 4,000

To Riya’s Capital A/c 3,000

To Siya’s Capital A/c 1,000