Page 165 - DEBKVOL-1

P. 165

Chapter 7 Death of a Partner 7.7

.

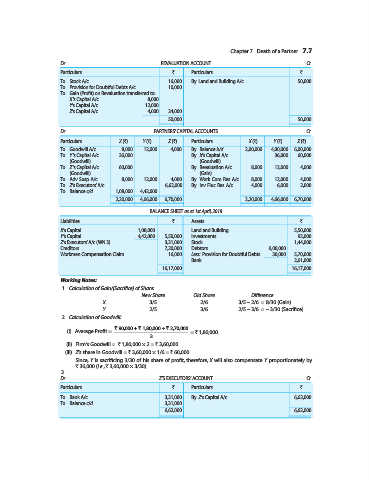

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Stock A/c 16,000 By Land and Building A/c 50,000

To Provision for Doubtful Debts A/c 10,000

To Gain (Profit) on Revaluation transferred to:

X’s Capital A/c 8,000

Y’s Capital A/c 12,000

Z’s Capital A/c 4,000 24,000

50,000 50,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X (`) Y (`) Z (`) Particulars X (`) Y (`) Z (`)

To Goodwill A/c 8,000 12,000 4,000 By Balance b/d 2,00,000 4,00,000 6,00,000

To Y’s Capital A/c 36,000 ... ... By X’s Capital A/c ... 36,000 60,000

(Goodwill) (Goodwill)

To Z’s Capital A/c 60,000 ... ... By Revaluation A/c 8,000 12,000 4,000

(Goodwill) (Gain)

To Adv. Susp. A/c 8,000 12,000 4,000 By Work. Com. Res. A/c 8,000 12,000 4,000

To Z’s Executors’ A/c ... ... 6,62,000 By Inv. Fluc. Res. A/c 4,000 6,000 2,000

To Balance c/d 1,08,000 4,42,000 ...

2,20,000 4,66,000 6,70,000 2,20,000 4,66,000 6,70,000

BALANCE SHEET as at 1st April, 2018

Liabilities ` Assets `

X’s Capital 1,08,000 Land and Building 5,50,000

Y’s Capital 4,42,000 5,50,000 Investments 92,000

Z’s Executors’ A/c (WN 3) 3,31,000 Stock 1,44,000

Creditors 7,20,000 Debtors 6,00,000

Workmen Compensation Claim 16,000 Less: Provision for Doubtful Debts 30,000 5,70,000

Bank 2,61,000

16,17,000 16,17,000

Working Notes:

1. Calculation of Gain/(Sacrifice) of Share:

New Share Old Share Difference

X 3/5 2/6 3/5 – 2/6 = 8/30 (Gain)

Y 2/5 3/6 2/5 – 3/6 = – 3/30 (Sacrifice)

2. Calculation of Goodwill:

` 90,000 + 1,80,000 + 2,70,000` `

(i) Average Profit = = ` 1,80,000.

3

(ii) Firm's Goodwill = ` 1,80,000 × 2 = ` 3,60,000.

(iii) Z’s share in Goodwill = ` 3,60,000 × 1/6 = ` 60,000.

Since, Y is sacrificing 3/30 of his share of profit, therefore, X will also compensate Y proportionately by

` 36,000 (i.e., ` 3,60,000 × 3/30).

3.

Dr. Z’S EXECUTORS’ ACCOUNT Cr.

Particulars ` Particulars `

To Bank A/c 3,31,000 By Z’s Capital A/c 6,62,000

To Balance c/d 3,31,000

6,62,000 6,62,000