Page 311 - AAAXII

P. 311

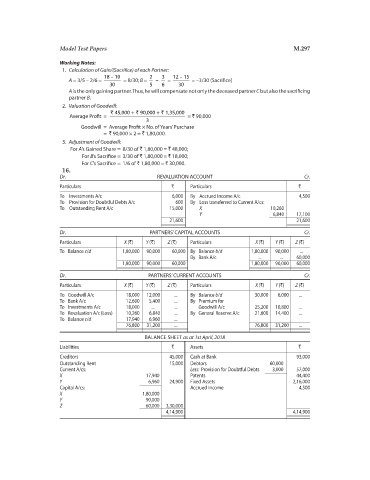

Model Test Papers M.297

Working Notes:

1. Calculation of Gain/(Sacrifice) of each Partner:

18 – 10 2 3 12 – 15

A = 3/5 – 2/6 = = 8/30; B = – = = –3/30 (Sacrifice)

30 5 6 30

A is the only gaining partner. Thus, he will compensate not only the deceased partner C but also the sacrificing

partner B.

2. Valuation of Goodwill:

` 45,000 + 90,000 + 1,35,000` `

Average Profit = = ` 90,000

3

Goodwill = Average Profit × No. of Years’ Purchase

= ` 90,000 × 2 = ` 1,80,000.

3. Adjustment of Goodwill:

For A’s Gained Share = 8/30 of ` 1,80,000 = ` 48,000;

For B’s Sacrifice = 3/30 of ` 1,80,000 = ` 18,000;

For C’s Sacrifice = 1/6 of ` 1,80,000 = ` 30,000.

16.

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Investments A/c 6,000 By Accrued Income A/c 4,500

To Provision for Doubtful Debts A/c 600 By Loss transferred to Current A/cs:

To Outstanding Rent A/c 15,000 X 10,260

Y 6,840 17,100

21,600 21,600

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X (`) Y (`) Z (`) Particulars X (`) Y (`) Z (`)

To Balance c/d 1,80,000 90,000 60,000 By Balance b/d 1,80,000 90,000 ...

By Bank A/c ... ... 60,000

1,80,000 90,000 60,000 1,80,000 90,000 60,000

Dr. PARTNERS’ CURRENT ACCOUNTS Cr.

Particulars X (`) Y (`) Z (`) Particulars X (`) Y (`) Z (`)

To Goodwill A/c 18,000 12,000 ... By Balance b/d 30,000 6,000 ...

To Bank A/c 12,600 5,400 ... By Premium for

To Investments A/c 18,000 ... ... Goodwill A/c 25,200 10,800 ...

To Revaluation A/c (Loss) 10,260 6,840 ... By General Reserve A/c 21,600 14,400 ...

To Balance c/d 17,940 6,960 ...

76,800 31,200 ... 76,800 31,200 ...

BALANCE SHEET as at 1st April, 2018

Liabilities ` Assets `

Creditors 45,000 Cash at Bank 93,000

Outstanding Rent 15,000 Debtors 60,000

Current A/cs: Less: Provision for Doubtful Debts 3,000 57,000

X 17,940 Patents 44,400

Y 6,960 24,900 Fixed Assets 2,16,000

Capital A/cs: Accrued Income 4,500

X 1,80,000

Y 90,000

Z 60,000 3,30,000

4,14,900 4,14,900