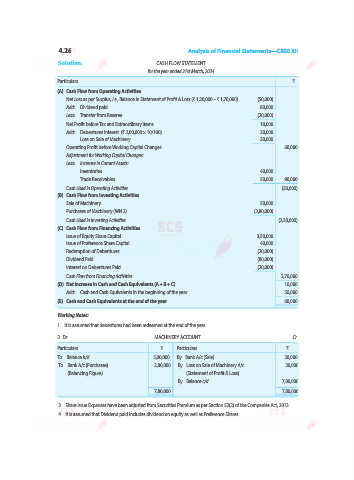

Page 108 - afs12

P. 108

5.8 Analysis of Financial Statements—CBSE XII

3. Dr. ACCUMULATED DEPRECIATION ACCOUNT Cr.

Particulars ` Particulars `

To Property, Plant and Equipment A/c (Transfer) 30,000 By Balance b/d 2,12,500

To Balance c/d 2,20,000 By Depreciation A/c (Bal. Fig.) 37,500

2,50,000 2,50,000

Illustration 5. Calculate Cash Flow from Financing Activities from the following:

Particulars 31st March, 31st March,

2024 (`) 2025 (`)

Equity Share Capital 6,00,000 8,00,000

12% Preference Share Capital 2,00,000 ...

10% Debentures ... 1,00,000

Additional Information:

1. Equity shares were issued at a premium of 15%, underwriting commission paid thereon

` 10,000.

2. 12% Preference shares were redeemed at a premium of 5%.

3. 10% Debentures were issued at a discount of 10%.

4. Interest paid on debentures ` 10,000.

5. Dividend paid on preference shares ` 24,000.

6. Interim dividend paid on equity shares ` 64,000.

Solution: CASH FLOW FROM FINANCING ACTIVITIES

Particulars `

Issue of Equity Shares (` 2,00,000 + ` 30,000) 2,30,000

Redemption of 12% Preference Shares (` 2,00,000 + ` 10,000) (2,10,000)

Issue of 10% Debentures (` 1,00,000 – ` 10,000) 90,000

Underwriting Commission Paid (10,000)

Interest Paid on Debentures (10,000)

Dividend Paid on Preference Shares (24,000)

Interim Dividend Paid on Equity Shares (64,000)

Cash Flow from Financing Activities 2,000

Illustration 6. X Ltd. provides the following information, calculate the Net Cash

Flow from Investing Activities and Net Cash Flow from Financing Activities as per

AS-3 (Revised):

Particulars 31st March, 31st March,

2024 (`) 2025 (`)

8% Preference Share Capital 2,00,000 1,50,000

Equity Share Capital 5,00,000 10,00,000

11% Debentures 2,00,000 1,00,000

Securities Premium ... 50,000

Investment 1,00,000 2,50,000

Goodwill ... 1,00,000

Machinery 2,15,000 4,00,000

Patents 1,50,000 ...