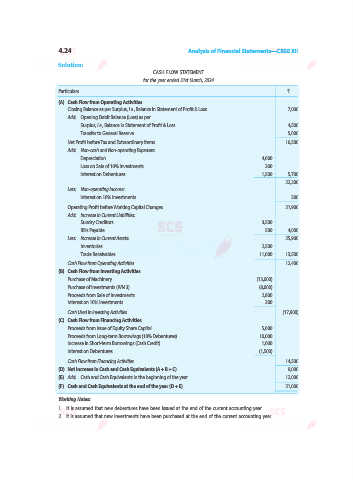

Page 106 - afs12

P. 106

5.6 Analysis of Financial Statements—CBSE XII

Solution:

Net Profit before Tax and Extraordinary Items: `

Surplus, i.e., Balance in Statement of Profit & Loss (Closing) 2,10,000

Less: Surplus, i.e., Balance in Statement of Profit & Loss (Opening) 1,40,000

70,000

Add: Transfer to General Reserve (` 1,20,000 – ` 80,000) 40,000

Dividend (Previous Year) Paid during the year 90,000

Provision for Tax (Current Year) 70,000

Net Profit before Tax and Extraordinary Items 2,70,000

Illustration 3. Calculate Cash Flow from Operating Activities from the following information:

`

Net Profit (After Provision for Tax ` 3,06,000) 14,06,000

Proposed Dividend 2,42,000

Above Net Profit is determined after following Credit and Debits:

Credits:

(i) Compensation for Earthquake Disaster 1,50,000

(ii) (Gain) Profit on Sale of Machinery 35,000

(iii) Dividend Received on Investments 30,000

Debits:

(i) Depreciation 2,80,000

(ii) Loss on Sale of Investments 60,000

Decrease or Increase in Current Assets and Current Liabilities is as follows:

Decrease in Current Assets (Other than Cash and Cash Equivalents) 20,000

Increase in Current Liabilities (Other than Bank Overdraft and Cash Credit) 3,02,000

Increase in Current Assets (Other than Cash and Cash Equivalents) 6,00,000

Decrease in Current Liabilities (Other than Bank Overdraft and Cash Credit) 1,28,000

Other Information:

Income Tax Paid 2,36,000

Refund of Income Tax Received 6,000

Solution: CASH FLOW FROM OPERATING ACTIVITIES

Particulars `

Net Profit After Tax 14,06,000

Add: Provision for Tax 3,06,000

17,12,000

Less: Refund of Income Tax 6,000

Extraordinary Items: Compensation for Earthquake Disaster 1,50,000 1,56,000

Net Profit before Tax and Extraordinary Items 15,56,000

Add: Non-Cash/Non-Operating Items:

Depreciation 2,80,000

Loss on Sale of Investments 60,000

Less: Non-Cash/Non-Operating Items:

Gain (Profit) on Sale of Machinery (35,000)

Dividend Received on Investments (30,000)

Operating Profit before Working Capital Changes 18,31,000

Add: Decrease in Current Assets 20,000

Increase in Current Liabilities 3,02,000

21,53,000

Less: Increase in Current Assets (6,00,000)

Decrease in Current Liabilities (1,28,000) (7,28,000)

Cash Flow from Operating Activities before Tax and Extraordinary Items 14,25,000

Less: Income Tax Paid (Net of Refund) (2,30,000)

Cash Flow from Operating Activities after Tax 11,95,000

Add: Extraordinary Item: Compensation for Earthquake Disaster 1,50,000

Cash Flow from Operating Activities 13,45,000

Note: Proposed Dividend is not taken as the Net Profit given is after Provision for Tax.