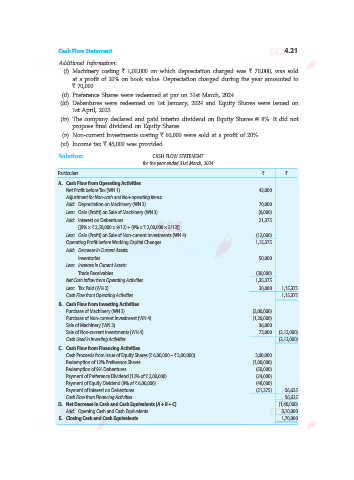

Page 103 - afs12

P. 103

Cash Flow Statement 5.3

(F) Less: Increase in Current Assets and

Decrease in Current Liabilities

— Increase in Inventories (Stock) ...

— Increase in Trade Receivables (Debtors/Bills Receivable) ...

— Increase in Accrued Incomes ...

— Increase in Prepaid Expenses ...

— Decrease in Trade Payables (Creditors/Bills Payable) ...

— Decrease in Outstanding Expenses ...

— Decrease in Advance Incomes ... ...

(G) Cash Generated from Operations (D + E – F) ...

(H) Less: Income Tax Paid (Net of Tax Refund received) ...

(I) Cash Flow before Extraordinary Items ...

— Extraordinary Items (+/–) ...

(J) Cash Flow from (or Used in) Operating Activities ...

II. Cash Flow from Investing Activities

— Proceeds from Sale of Fixed Assets ...

— Proceeds from Sale of Investments (Other than Current Investments (to be

included in Cash and Cash Equivalents) and Marketable Securities) ...

— Proceeds from Sale of Intangible Assets ...

— Interest and Dividend received (For Non-financial Companies only) ...

— Rent Received ...

— Payment for Purchase of Fixed Assets (...)

— Payment for Purchase of Investments (Other than Marketable Securities) (...)

— Payment for Purchase of Intangible Assets like Goodwill (...)

— Extraordinary Items (e.g., Insurance Claim on Machinery against Fire) (+/–) ...

Cash Flow from (or Used in) Investing Activities ...

III. Cash Flow from Financing Activities

— Proceeds from Issue of Shares and Debentures ...

— Proceeds from Other Long-term Borrowings ...

— Increase/Decrease in Bank Overdraft and Cash Credit ...

— Final Dividend paid during the year (...)

— Interim Dividend paid during the year (...)

— Payment of Interest on Debentures and Loans (Short-term and Long-term) (...)

— Repayment of Loans (...)

— Redemption of Debentures/Preference Shares (...)

— Payment of Share Issue Expenses (...)

— Payment for Buy-back of Shares as Extraordinary Activity (...)

Cash Flow from (or Used in) Financing Activities ...

IV. Net Increase/Decrease in Cash and Cash Equivalents (I + II + III) ...

V. Add: Cash and Cash Equivalents in the beginning of the year

— Cash-in-Hand ...

— Cash at Bank ...

— Short-term Deposits ...

— Current Investments ...

— Marketable Securities ... ...

...

VI. Cash and Cash Equivalents at the end of the year

— Cash-in-Hand ...

— Cash at Bank ...

— Short-term Deposits ...

— Current Investments ...

— Marketable Securities ... ...

*Alternatively, increase/decrease in Provision for Doubtful Debts may be treated under increase/decrease in

Current Liabilities. In this situation, increase/decrease in Provision for Doubtful Debts is adjusted after Operating

Profit before Working Capital Changes.