Page 104 - afs12

P. 104

5.4 Analysis of Financial Statements—CBSE XII

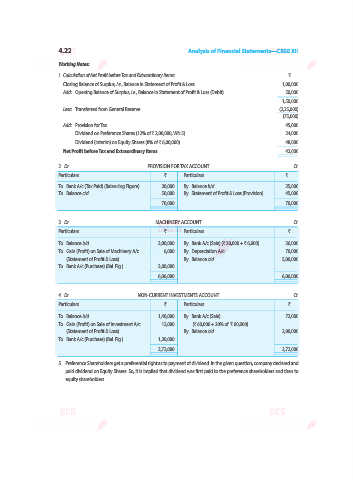

Working Note: Net Profit before Tax and Extraordinary Items: `

Net Profit as per Statement of Profit & Loss or Difference between Closing Balance and

Opening Balance of Surplus, i.e., Balance in Statement of Profit & Loss ...

Add: Transfer to Reserves ...

Dividend (Proposed Dividend of previous year) paid during the year ...

Interim Dividend paid during the year ...

Provision for Tax for the current year ...

Extraordinary Items, if any, debited to the Statement of Profit & Loss ...

...

Less: Extraordinary Items, if any, credited to the Statement of Profit & Loss ...

Refund of Tax credited to the Statement of Profit & Loss ... ...

Net Profit before Tax and Extraordinary Items ...

IMPORTANT NOTE

1. Current Investments to be taken as Marketable Securities unless otherwise specified.

2. Bank overdraft and cash credit is treated as short-term Borrowings.

Solved Questions

Illustration 1. Following relevant information is obtained from the books of X Ltd.:

Particulars Note No. 31st March, 31st March,

2025 (`) 2024 (`)

I. EQUITY AND LIABILITIES

Short-term Provision: Provision for Tax 70,000 50,000

The amount of tax paid during 2024–25 amounted to ` 40,000. How would you deal

with this item while preparing Cash Flow Statement? You are also given net profit after

taxation ` 80,000.

Solution:

Dr. PROVISION FOR TAX ACCOUNT Cr.

Particulars ` Particulars `

To Bank A/c (Tax Paid) 40,000 By Balance b/d 50,000

To Balance c/d 70,000 By Statement of Profit & Loss (Bal. Fig.) 60,000

(Tax Provided)

1,10,000 1,10,000

Note: If Opening and Closing amounts of Provision for Tax are given with the figure of tax paid (provided)

during the year, prepare Provision for Tax Account to ascertain the amount of tax provided (paid) during the

current year.