Page 154 - afs12

P. 154

5.54 Analysis of Financial Statements—CBSE XII

(ii) Bank loan was repaid and Preference Shares were redeemed at par on 31st March, 2025.

(iii) Debentures were redeemed on 1st January, 2025 and Equity Shares were issued on 1st April, 2024.

(iv) During the year, company declared and paid interim dividend on Equity Shares @ 8%. Final dividend

was not proposed on equity shares.

(v) At the end of the year some Non-current Investments costing ` 60,000 were sold at a profit of 20%.

Some of Non-current investments were also made on 31st March, 2025.

(vi) Tax paid during the year was ` 1,40,000 and adjusted against Provision for Tax Account.

(vii) Proposed dividend for the year ended 31st March, 2024 ` 24,000 was paid during the year.

[Ans.: Cash Flow from Operating Activities = ` 3,36,375; Cash Used in Investing Activities = ` 2,98,000;

Cash Used to Financing Activities = ` 1,03,375; Net Decrease in Cash and Cash Equivalents = ` 65,000.]

21. From the following extract of Balance Sheet of a company, calculate Cash Flow from Financing Activities:

Particulars 31st March, 31st March,

2025 (`) 2024 (`)

Equity Share Capital 6,00,000 4,00,000

10% Preference Share Capital 2,00,000 3,00,000

Securities Premium 35,000 ...

11% Debentures 5,00,000 4,00,000

Additional Information:

(i) Equity shares were issued at a premium of 20% on 31st March, 2025.

(ii) Underwriting commission on issue of equity shares ` 5,000. The company met underwriting commission

from Securities Premium.

(iii) Preference shares were redeemed on 31st March, 2025 at par along with dividend.

(iv) Additional Debentures were issued on 1st April, 2024.

(v) The company paid interim dividend @ 9% on Equity Share Capital. The company did not propose

final dividend on Equity share Capital.

[Ans.: Cash Flow from Financing Activities = ` 1,14,000.]

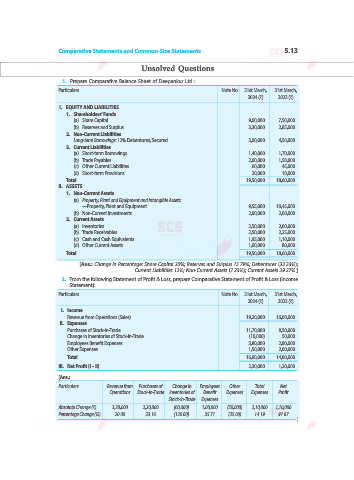

22. Following are the Balance Sheets of Sreshtha Ltd. as on 31st March, 2025 and 2024:

Particulars Note No. 31st March, 31st March,

2025 (`) 2024 (`)

I. EQUITY AND LIABILITIES

1. Shareholders’ Funds

(a) Share Capital 40,00,000 30,00,000

(b) Reserves and Surplus 1 10,00,000 6,00,000

2. Non-Current Liabilities

Long-term Borrowings 6,00,000 4,00,000

3. Current Liabilities

(a) Trade Payables 3,00,000 4,00,000

(b) Short-term Provisions 2 1,40,000 1,20,000

Total 60,40,000 45,20,000

II. ASSETS

1. Non-Current Assets

Property, Plant and Equipment and Intangible Assets:

(i) Property, Plant and Equipment 3 38,00,000 30,00,000

(ii) Intangible Assets 4 9,40,000 5,40,000

2. Current Assets

(a) Inventories 5,00,000 3,20,000

(b) Trade Receivables 4,20,000 4,20,000

(c) Cash and Cash Equivalents 3,80,000 2,40,000

Total 60,40,000 45,20,000