Page 39 - DEBK11

P. 39

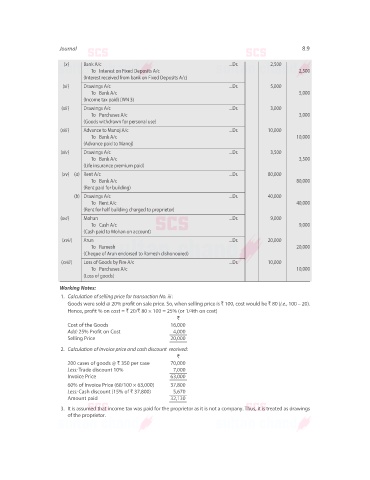

Journal 8.9

(x) Bank A/c ...Dr. 2,500

To Interest on Fixed Deposits A/c 2,500

(Interest received from bank on Fixed Deposits A/c)

(xi) Drawings A/c ...Dr. 5,000

To Bank A/c 5,000

(Income tax paid) (WN 3)

(xii) Drawings A/c ...Dr. 3,000

To Purchases A/c 3,000

(Goods withdrawn for personal use)

(xiii) Advance to Manoj A/c ...Dr. 10,000

To Bank A/c 10,000

(Advance paid to Manoj)

(xiv) Drawings A/c ...Dr. 3,500

To Bank A/c 3,500

(Life insurance premium paid)

(xv) (a) Rent A/c ...Dr. 80,000

To Bank A/c 80,000

(Rent paid for building)

(b) Drawings A/c ...Dr. 40,000

To Rent A/c 40,000

(Rent for half building charged to proprietor)

(xvi) Mohan ...Dr. 9,000

To Cash A/c 9,000

(Cash paid to Mohan on account)

(xvii) Arun ...Dr. 20,000

To Ramesh 20,000

(Cheque of Arun endorsed to Ramesh dishonoured)

(xviii) Loss of Goods by Fire A/c ...Dr. 10,000

To Purchases A/c 10,000

(Loss of goods)

Working Notes:

1. Calculation of selling price for transaction No. iii:

Goods were sold @ 20% profit on sale price. So, when selling price is ` 100, cost would be ` 80 (i.e., 100 – 20).

Hence, profit % on cost = ` 20/` 80 × 100 = 25% (or 1/4th on cost)

`

Cost of the Goods 16,000

Add: 25% Profit on Cost 4,000

Selling Price 20,000

2. Calculation of invoice price and cash discount received:

`

200 cases of goods @ ` 350 per case 70,000

Less: Trade discount 10% 7,000

Invoice Price 63,000

60% of Invoice Price (60/100 × 63,000) 37,800

Less: Cash discount (15% of ` 37,800) 5,670

Amount paid 32,130

3. It is assumed that income tax was paid for the proprietor as it is not a company. Thus, it is treated as drawings

of the proprietor.