Page 121 - ISCDEBK-XI

P. 121

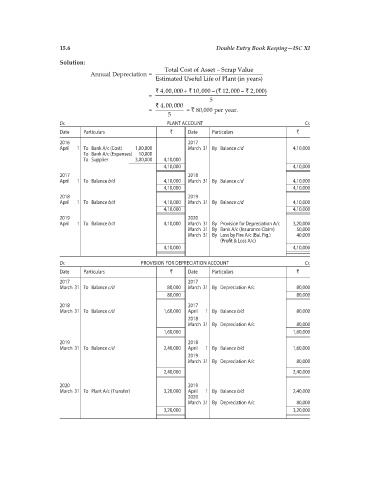

15.6 Double Entry Book Keeping—ISC XI

Solution:

Total Cost of Asset Scrap Value

Annual Depreciation =

Estimated Useful Life of Plant (in years)

` 4,00,000 ` 10,000 ( 12,000 ` 2,000)

`

= 5

` 4,00,000

= = ` 80,000 per year.

5

Dr. PLANT ACCOUNT Cr.

Date Particulars ` Date Particulars `

2016 2017

April 1 To Bank A/c (Cost) 1,00,000 March 31 By Balance c/d 4,10,000

To Bank A/c (Expenses) 10,000

To Supplier 3,00,000 4,10,000

4,10,000 4,10,000

2017 2018

April 1 To Balance b/d 4,10,000 March 31 By Balance c/d 4,10,000

4,10,000 4,10,000

2018 2019

April 1 To Balance b/d 4,10,000 March 31 By Balance c/d 4,10,000

4,10,000 4,10,000

2019 2020

April 1 To Balance b/d 4,10,000 March 31 By Provision for Depreciation A/c 3,20,000

March 31 By Bank A/c (Insurance Claim) 50,000

March 31 By Loss by Fire A/c (Bal. Fig.) 40,000

(Profit & Loss A/c)

4,10,000 4,10,000

Dr. PROVISION FOR DEPRECIATION ACCOUNT Cr.

Date Particulars ` Date Particulars `

2017 2017

March 31 To Balance c/d 80,000 March 31 By Depreciation A/c 80,000

80,000 80,000

2018 2017

March 31 To Balance c/d 1,60,000 April 1 By Balance b/d 80,000

2018

March 31 By Depreciation A/c 80,000

1,60,000 1,60,000

2019 2018

March 31 To Balance c/d 2,40,000 April 1 By Balance b/d 1,60,000

2019

March 31 By Depreciation A/c 80,000

2,40,000 2,40,000

2020 2019

March 31 To Plant A/c (Transfer) 3,20,000 April 1 By Balance b/d 2,40,000

2020

March 31 By Depreciation A/c 80,000

3,20,000 3,20,000