Page 116 - ISCDEBK-12

P. 116

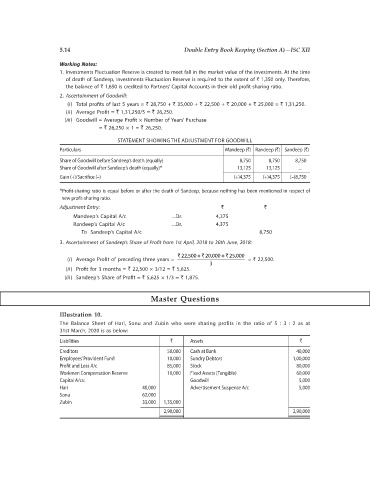

5.14 Double Entry Book Keeping (Section A)—ISC XII

Working Notes:

1. Investments Fluctuation Reserve is created to meet fall in the market value of the investments. At the time

of death of Sandeep, Investments Fluctuation Reserve is required to the extent of ` 1,350 only. Therefore,

the balance of ` 1,650 is credited to Partners’ Capital Accounts in their old profit-sharing ratio.

2. Ascertainment of Goodwill:

(i) Total profits of last 5 years = ` 28,750 + ` 35,000 + ` 22,500 + ` 20,000 + ` 25,000 = ` 1,31,250.

(ii) Average Profit = ` 1,31,250/5 = ` 26,250.

(iii) Goodwill = Average Profit × Number of Years’ Purchase

= ` 26,250 × 1 = ` 26,250.

STATEMENT SHOWING THE ADJUSTMENT FOR GOODWILL

Particulars Mandeep (`) Randeep (`) Sandeep (`)

Share of Goodwill before Sandeep’s death (equally) 8,750 8,750 8,750

Share of Goodwill after Sandeep’s death (equally)* 13,125 13,125 ...

Gain (+)/Sacrifice (–) (+)4,375 (+)4,375 (–)8,750

*Profit-sharing ratio is equal before or after the death of Sandeep, because nothing has been mentioned in respect of

new profit-sharing ratio.

Adjustment Entry: ` `

Mandeep’s Capital A/c ...Dr. 4,375

Randeep’s Capital A/c ...Dr. 4,375

To Sandeep’s Capital A/c 8,750

3. Ascertainment of Sandeep’s Share of Profit from 1st April, 2018 to 30th June, 2018:

` 22,500 + 20,000 + 25,000

`

`

(i) Average Profit of preceding three years = = ` 22,500.

3

(ii ) Profit for 3 months = ` 22,500 × 3/12 = ` 5,625.

(iii ) Sandeep’s Share of Profit = ` 5,625 × 1/3 = ` 1,875.

Master Questions

Illustration 10.

The Balance Sheet of Hari, Sonu and Zubin who were sharing profits in the ratio of 5 : 3 : 2 as at

31st March, 2020 is as below:

Liabilities ` Assets `

Creditors 50,000 Cash at Bank 40,000

Employees’ Provident Fund 10,000 Sundry Debtors 1,00,000

Profit and Loss A/c 85,000 Stock 80,000

Workmen Compensation Reserve 10,000 Fixed Assets (Tangible) 60,000

Capital A/cs: Goodwill 5,000

Hari 40,000 Advertisement Suspense A/c 5,000

Sonu 62,000

Zubin 33,000 1,35,000

2,90,000 2,90,000