Page 117 - ISCDEBK-12

P. 117

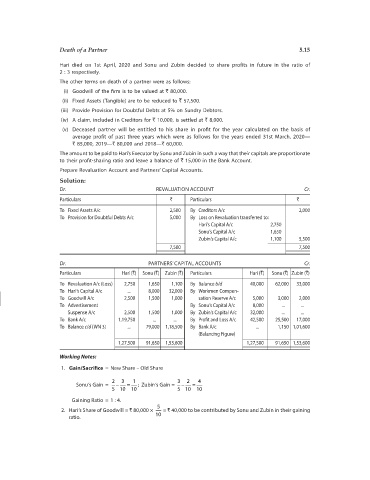

Death of a Partner 5.15

Hari died on 1st April, 2020 and Sonu and Zubin decided to share profits in future in the ratio of

2 : 3 respectively.

The other terms on death of a partner were as follows:

(i) Goodwill of the firm is to be valued at ` 80,000.

(ii) Fixed Assets (Tangible) are to be reduced to ` 57,500.

(iii) Provide Provision for Doubtful Debts at 5% on Sundry Debtors.

(iv) A claim, included in Creditors for ` 10,000, is settled at ` 8,000.

(v) Deceased partner will be entitled to his share in profit for the year calculated on the basis of

average profit of past three years which were as follows for the years ended 31st March, 2020—

` 85,000, 2019—` 80,000 and 2018—` 60,000.

The amount to be paid to Hari’s Executor by Sonu and Zubin in such a way that their capitals are proportionate

to their profit-sharing ratio and leave a balance of ` 15,000 in the Bank Account.

Prepare Revaluation Account and Partners’ Capital Accounts.

Solution:

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Fixed Assets A/c 2,500 By Creditors A/c 2,000

To Provision for Doubtful Debts A/c 5,000 By Loss on Revaluation transferred to:

Hari’s Capital A/c 2,750

Sonu’s Capital A/c 1,650

Zubin’s Capital A/c 1,100 5,500

7,500 7,500

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Hari (`) Sonu (`) Zubin (`) Particulars Hari (`) Sonu (`) Zubin (`)

To Revaluation A/c (Loss) 2,750 1,650 1,100 By Balance b/d 40,000 62,000 33,000

To Hari’s Capital A/c ... 8,000 32,000 By Workmen Compen-

To Goodwill A/c 2,500 1,500 1,000 sation Reserve A/c 5,000 3,000 2,000

To Advertisement By Sonu’s Capital A/c 8,000 ... ...

Suspense A/c 2,500 1,500 1,000 By Zubin’s Capital A/c 32,000 ... ...

To Bank A/c 1,19,750 ... ... By Profit and Loss A/c 42,500 25,500 17,000

To Balance c/d (WN 3) ... 79,000 1,18,500 By Bank A/c ... 1,150 1,01,600

(Balancing Figure)

1,27,500 91,650 1,53,600 1,27,500 91,650 1,53,600

Working Notes:

1. Gain/Sacrifice = New Share – Old Share

2 3 1 3 2 4

Sonu’s Gain = − = ; Zubin’s Gain = − =

5 10 10 5 10 10

Gaining Ratio = 1 : 4.

5

2. Hari’s Share of Goodwill = ` 80,000 × = ` 40,000 to be contributed by Sonu and Zubin in their gaining

ratio. 10