Page 147 - DEBKVOL-1

P. 147

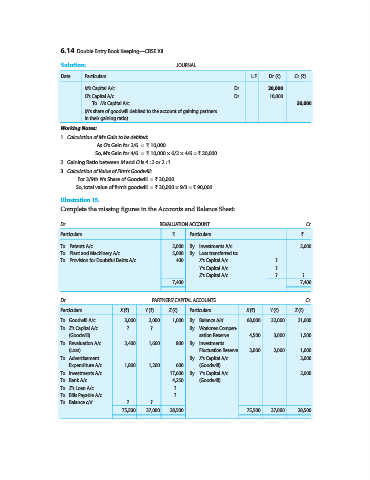

6.14 Double Entry Book Keeping—CBSE XII

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

M’s Capital A/c ...Dr. 20,000

O’s Capital A/c ...Dr. 10,000

To N’s Capital A/c 30,000

(N’s share of goodwill debited to the account of gaining partners

in their gaining ratio)

Working Notes:

1. Calculation of M’s Gain to be debited:

As O’s Gain for 2/6 = ` 10,000

So, M’s Gain for 4/6 = ` 10,000 × 6/2 × 4/6 = ` 20,000.

2. Gaining Ratio between M and O is 4 : 2 or 2 : 1.

3. Calculation of Value of Firm’s Goodwill:

For 3/9th N’s Share of Goodwill = ` 30,000

So, total value of firm’s goodwill = ` 30,000 × 9/3 = ` 90,000.

Illustration 15.

Complete the missing figures in the Accounts and Balance Sheet:

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Patents A/c 2,000 By Investments A/c 2,600

To Plant and Machinery A/c 5,000 By Loss transferred to:

To Provision for Doubtful Debts A/c 400 X’s Capital A/c ?

Y’s Capital A/c ?

Z’s Capital A/c ? ?

7,400 7,400

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X (`) Y (`) Z (`) Particulars X (`) Y (`) Z (`)

To Goodwill A/c 3,000 2,000 1,000 By Balance b/d 68,000 32,000 21,000

To Z’s Capital A/c ? ? By Workmen Compen-

(Goodwill) sation Reserve 4,500 3,000 1,500

To Revaluation A/c 2,400 1,600 800 By Investments

(Loss) Fluctuation Reserve 3,000 2,000 1,000

To Advertisement By X’s Capital A/c 3,000

Expenditure A/c 1,800 1,200 600 (Goodwill)

To Investments A/c 17,600 By Y’s Capital A/c 2,000

To Bank A/c 4,250 (Goodwill)

To Z’s Loan A/c ?

To Bills Payable A/c ?

To Balance c/d ? ?

75,500 37,000 28,500 75,500 37,000 28,500