Page 19 - DEBKVOL-1

P. 19

Chapter 1 Financial Statements of Not-for-Profit Organisations 1.9

.

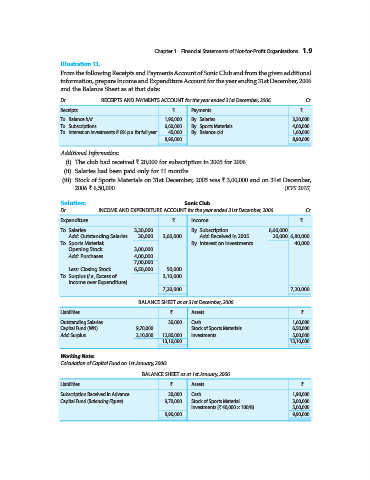

Illustration 11.

From the following Receipts and Payments Account of Sonic Club and from the given additional

information, prepare Income and Expenditure Account for the year ending 31st December, 2006

and the Balance Sheet as at that date:

Dr. RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st December, 2006 Cr.

Receipts ` Payments `

To Balance b/d 1,90,000 By Salaries 3,30,000

To Subscriptions 6,60,000 By Sports Materials 4,00,000

To Interest on Investments @ 8% p.a. for full year 40,000 By Balance c/d 1,60,000

8,90,000 8,90,000

Additional Information:

(i) The club had received ` 20,000 for subscription in 2005 for 2006.

(ii) Salaries had been paid only for 11 months.

(iii) Stock of Sports Materials on 31st December, 2005 was ` 3,00,000 and on 31st December,

2006 ` 6,50,000. (KVS 2015)

Solution: Sonic Club

Dr. INCOME AND EXPENDITURE ACCOUNT for the year ended 31st December, 2006 Cr.

Expenditure ` Income `

To Salaries 3,30,000 By Subscription 6,60,000

Add: Outstanding Salaries 30,000 3,60,000 Add: Received in 2005 20,000 6,80,000

To Sports Material: By Interest on Investments 40,000

Opening Stock 3,00,000

Add: Purchases 4,00,000

7,00,000

Less: Closing Stock 6,50,000 50,000

To Surplus (i.e., Excess of 3,10,000

Income over Expenditure)

7,20,000 7,20,000

BALANCE SHEET as at 31st December, 2006

Liabilities ` Assets `

Outstanding Salaries 30,000 Cash 1,60,000

Capital Fund (WN) 9,70,000 Stock of Sports Materials 6,50,000

Add: Surplus 3,10,000 12,80,000 Investments 5,00,000

13,10,000 13,10,000

Working Note:

Calculation of Capital Fund on 1st January, 2006:

BALANCE SHEET as at 1st January, 2006

Liabilities ` Assets `

Subscription Received in Advance 20,000 Cash 1,90,000

Capital Fund (Balancing Figure) 9,70,000 Stock of Sports Material 3,00,000

Investments (` 40,000 × 100/8) 5,00,000

9,90,000 9,90,000