Page 198 - DEBKVOL-1

P. 198

Chapter 8 Dissolution of a Partnership Firm 8.23

.

Additional Information:

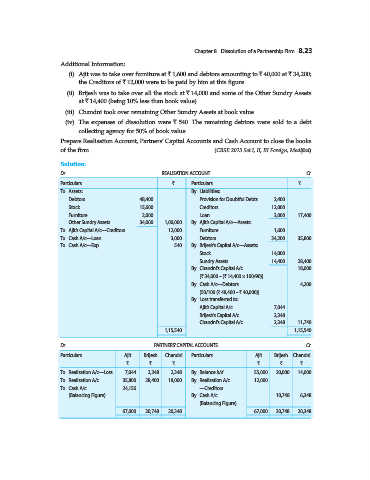

(i) Ajit was to take over furniture at ` 1,600 and debtors amounting to ` 40,000 at ` 34,200;

the Creditors of ` 12,000 were to be paid by him at this figure.

(ii) Brijesh was to take over all the stock at ` 14,000 and some of the Other Sundry Assets

at ` 14,400 (being 10% less than book value).

(iii) Chandni took over remaining Other Sundry Assets at book value.

(iv) The expenses of dissolution were ` 540. The remaining debtors were sold to a debt

collecting agency for 50% of book value.

Prepare Realisation Account, Partners’ Capital Accounts and Cash Account to close the books

of the firm. (CBSE 2013 Set I, II, III Foreign, Modified)

Solution:

Dr. REALISATION ACCOUNT Cr.

Particulars ` Particulars `

To Assets: By Liabilities:

Debtors 48,400 Provision for Doubtful Debts 2,400

Stock 15,600 Creditors 12,000

Furniture 2,000 Loan 3,000 17,400

Other Sundry Assets 34,000 1,00,000 By Ajit’s Capital A/c—Assets:

To Ajit’s Capital A/c—Creditors 12,000 Furniture 1,600

To Cash A/c—Loan 3,000 Debtors 34,200 35,800

To Cash A/c—Exp. 540 By Brijesh’s Capital A/c—Assets:

Stock 14,000

Sundry Assets 14,400 28,400

By Chandni’s Capital A/c 18,000

[` 34,000 – (` 14,400 × 100/90)]

By Cash A/c—Debtors 4,200

[50/100 (` 48,400 – ` 40,000)]

By Loss transferred to:

Ajit’s Capital A/c 7,044

Brijesh’s Capital A/c 2,348

Chandni’s Capital A/c 2,348 11,740

1,15,540 1,15,540

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Ajit Brijesh Chandni Particulars Ajit Brijesh Chandni

` ` ` ` ` `

To Realisation A/c—Loss 7,044 2,348 2,348 By Balance b/d 55,000 20,000 14,000

To Realisation A/c 35,800 28,400 18,000 By Realisation A/c 12,000 ... ...

To Cash A/c 24,156 ... ... —Creditors

(Balancing Figure) By Cash A/c ... 10,748 6,348

(Balancing Figure)

67,000 30,748 20,348 67,000 30,748 20,348