Page 195 - DEBKVOL-1

P. 195

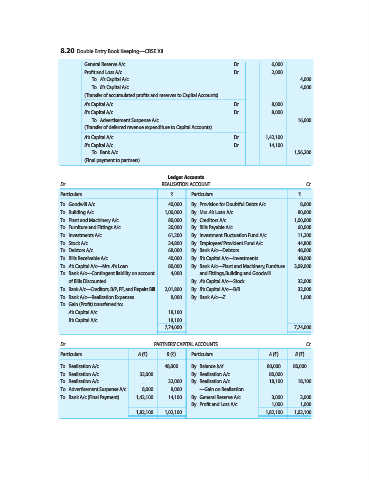

8.20 Double Entry Book Keeping—CBSE XII

General Reserve A/c ...Dr. 6,000

Profit and Loss A/c ...Dr. 2,000

To A’s Capital A/c 4,000

To B’s Capital A/c 4,000

(Transfer of accumulated profits and reserves to Capital Accounts)

A’s Capital A/c ...Dr. 8,000

B’s Capital A/c ...Dr. 8,000

To Advertisement Suspense A/c 16,000

(Transfer of deferred revenue expenditure to Capital Accounts)

A‘s Capital A/c ...Dr. 1,42,100

B’s Capital A/c ...Dr. 14,100

To Bank A/c 1,56,200

(Final payment to partners)

Ledger Accounts

Dr. REALISATION ACCOUNT Cr.

Particulars ` Particulars `

To Goodwill A/c 40,000 By Provision for Doubtful Debts A/c 8,000

To Building A/c 1,00,000 By Mrs. A’s Loan A/c 80,000

To Plant and Machinery A/c 80,000 By Creditors A/c 1,00,000

To Furniture and Fittings A/c 20,000 By Bills Payable A/c 60,000

To Investments A/c 61,200 By Investment Fluctuation Fund A/c 11,200

To Stock A/c 34,800 By Employees’ Provident Fund A/c 44,800

To Debtors A/c 68,000 By Bank A/c—Debtors 48,000

To Bills Receivable A/c 40,000 By B’s Capital A/c—Investments 48,000

To A’s Capital A/c—Mrs. A’s Loan 80,000 By Bank A/c—Plant and Machinery, Furniture 3,09,000

To Bank A/c—Contingent liability on account 4,000 and Fittings, Building and Goodwill

of Bills Discounted By A’s Capital A/c—Stock 32,000

To Bank A/c—Creditors, B/P, PF, and Repairs Bill 2,01,800 By B’s Capital A/c—B/R 32,000

To Bank A/c—Realisation Expenses 8,000 By Bank A/c—Z 1,000

To Gain (Profit) transferred to:

A’s Capital A/c 18,100

B‘s Capital A/c 18,100

7,74,000 7,74,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars A (`) B (`) Particulars A (`) B (`)

To Realisation A/c ... 48,000 By Balance b/d 80,000 80,000

To Realisation A/c 32,000 ... By Realisation A/c 80,000 ...

To Realisation A/c ... 32,000 By Realisation A/c 18,100 18,100

To Advertisement Suspense A/c 8,000 8,000 —Gain on Realisation

To Bank A/c (Final Payment) 1,42,100 14,100 By General Reserve A/c 3,000 3,000

By Profit and Loss A/c 1,000 1,000

1,82,100 1,02,100 1,82,100 1,02,100