Page 194 - DEBKVOL-1

P. 194

Chapter 8 Dissolution of a Partnership Firm 8.19

.

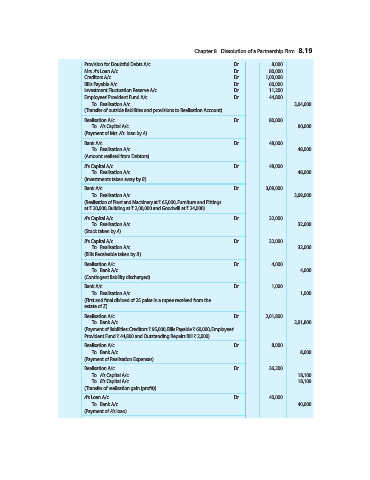

Provision for Doubtful Debts A/c ...Dr. 8,000

Mrs. A’s Loan A/c ...Dr. 80,000

Creditors A/c ...Dr. 1,00,000

Bills Payable A/c ...Dr. 60,000

Investment Fluctuation Reserve A/c ...Dr. 11,200

Employees’ Provident Fund A/c ...Dr. 44,800

To Realisation A/c 3,04,000

(Transfer of outside liabilities and provisions to Realisation Account)

Realisation A/c ...Dr. 80,000

To A’s Capital A/c 80,000

(Payment of Mrs. A’s loan by A)

Bank A/c ...Dr. 48,000

To Realisation A/c 48,000

(Amount realised from Debtors)

B’s Capital A/c ...Dr. 48,000

To Realisation A/c 48,000

(Investments taken away by B)

Bank A/c ...Dr. 3,09,000

To Realisation A/c 3,09,000

(Realisation of Plant and Machinery at ` 65,000, Furniture and Fittings

at ` 20,000, Building at ` 2,00,000 and Goodwill at ` 24,000)

A’s Capital A/c ...Dr. 32,000

To Realisation A/c 32,000

(Stock taken by A)

B’s Capital A/c ...Dr. 32,000

To Realisation A/c 32,000

(Bills Receivable taken by B)

Realisation A/c ...Dr. 4,000

To Bank A/c 4,000

(Contingent liability discharged)

Bank A/c ...Dr. 1,000

To Realisation A/c 1,000

(First and final divined of 25 paise in a rupee received from the

estate of Z)

Realisation A/c ...Dr. 2,01,800

To Bank A/c 2,01,800

(Payment of liabilities: Creditors ` 95,000, Bills Payable ` 60,000, Employees’

Provident Fund ` 44,800 and Outstanding Repairs Bill ` 2,000)

Realisation A/c ...Dr. 8,000

To Bank A/c 8,000

(Payment of Realisation Expenses)

Realisation A/c ...Dr. 36,200

To A’s Capital A/c 18,100

To B’s Capital A/c 18,100

(Transfer of realisation gain (profit))

A’s Loan A/c ...Dr. 40,000

To Bank A/c 40,000

(Payment of A’s loan)