Page 197 - DEBKVOL-1

P. 197

8.22 Double Entry Book Keeping—CBSE XII

Solution:

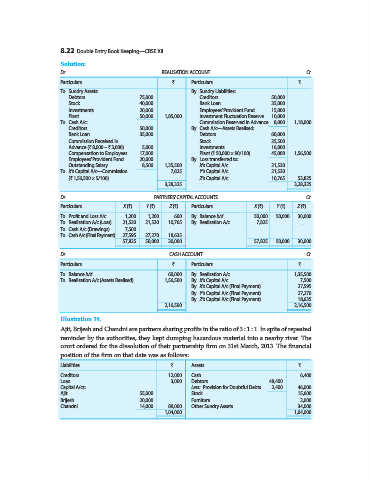

Dr. REALISATION ACCOUNT Cr.

Particulars ` Particulars `

To Sundry Assets: By Sundry Liabilities:

Debtors 75,000 Creditors 50,000

Stock 40,000 Bank Loan 35,000

Investments 20,000 Employees’ Provident Fund 15,000

Plant 50,000 1,85,000 Investment Fluctuation Reserve 10,000

To Cash A/c: Commission Reserved in Advance 8,000 1,18,000

Creditors 50,000 By Cash A/c—Assets Realised:

Bank Loan 35,000 Debtors 60,000

Commission Received in Stock 35,500

Advance (` 8,000 – ` 3,000) 5,000 Investments 16,000

Compensation to Employees 17,000 Plant (` 50,000 × 90/100) 45,000 1,56,500

Employees’ Provident Fund 20,000 By Loss transferred to:

Outstanding Salary 8,500 1,35,500 X’s Capital A/c 21,530

To X’s Capital A/c—Commission 7,825 Y’s Capital A/c 21,530

(` 1,56,500 × 5/100) Z’s Capital A/c 10,765 53,825

3,28,325 3,28,325

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X (`) Y (`) Z (`) Particulars X (`) Y (`) Z (`)

To Profit and Loss A/c 1,200 1,200 600 By Balance b/d 50,000 50,000 30,000

To Realisation A/c (Loss) 21,530 21,530 10,765 By Realisation A/c 7,825 ... ...

To Cash A/c (Drawings) 7,500 ... ...

To Cash A/c (Final Payment) 27,595 27,270 18,635

57,825 50,000 30,000 57,825 50,000 30,000

Dr. CASH ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 60,000 By Realisation A/c 1,35,500

To Realisation A/c (Assets Realised) 1,56,500 By X’s Capital A/c 7,500

By X’s Capital A/c (Final Payment) 27,595

By Y’s Capital A/c (Final Payment) 27,270

By Z’s Capital A/c (Final Payment) 18,635

2,16,500 2,16,500

Illustration 19.

Ajit, Brijesh and Chandni are partners sharing profits in the ratio of 3 : 1 : 1. In spite of repeated

reminder by the authorities, they kept dumping hazardous material into a nearby river. The

court ordered for the dissolution of their partnership firm on 31st March, 2013. The financial

position of the firm on that date was as follows:

Liabilities ` Assets `

Creditors 12,000 Cash 6,400

Loan 3,000 Debtors 48,400

Capital A/cs: Less: Provision for Doubtful Debts 2,400 46,000

Ajit 55,000 Stock 15,600

Brijesh 20,000 Furniture 2,000

Chandni 14,000 89,000 Other Sundry Assets 34,000

1,04,000 1,04,000