Page 205 - DEBKVOL-1

P. 205

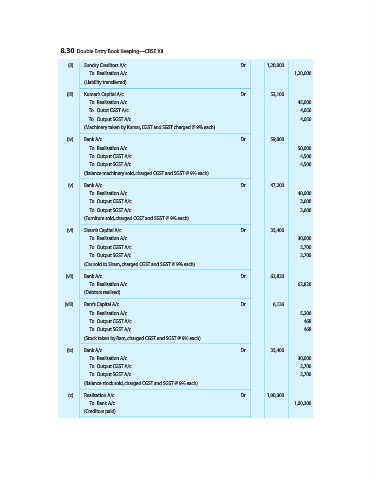

8.30 Double Entry Book Keeping—CBSE XII

(ii) Sundry Creditors A/c ...Dr. 1,20,000

To Realisation A/c 1,20,000

(Liability transferred)

(iii) Kumar’s Capital A/c ...Dr. 53,100

To Realisation A/c 45,000

To Outut CGST A/c 4,050

To Output SGST A/c 4,050

(Machinery taken by Kumar, CGST and SGST charged @ 9% each)

(iv) Bank A/c ...Dr. 59,000

To Realisation A/c 50,000

To Output CGST A/c 4,500

To Output SGST A/c 4,500

(Balance machinery sold, charged CGST and SGST @ 9% each)

(v) Bank A/c ...Dr. 47,200

To Realisation A/c 40,000

To Output CGST A/c 3,600

To Output SGST A/c 3,600

(Furniture sold, charged CGST and SGST @ 9% each)

(vi) Sham’s Capital A/c ...Dr. 35,400

To Realisation A/c 30,000

To Output CGST A/c 2,700

To Output SGST A/c 2,700

(Car sold to Sham, charged CGST and SGST @ 9% each)

(vii) Bank A/c ...Dr. 62,820

To Realisation A/c 62,820

(Debtors realised)

(viii) Ram’s Capital A/c ...Dr. 6,136

To Realisation A/c 5,200

To Output CGST A/c 468

To Output SGST A/c 468

(Stock taken by Ram, charged CGST and SGST @ 9% each)

(ix) Bank A/c ...Dr. 35,400

To Realisation A/c 30,000

To Output CGST A/c 2,700

To Output SGST A/c 2,700

(Balance stock sold, charged CGST and SGST @ 9% each)

(x) Realisation A/c ...Dr. 1,00,300

To Bank A/c 1,00,300

(Creditors paid)