Page 206 - DEBKVOL-1

P. 206

Chapter 8 Dissolution of a Partnership Firm 8.31

.

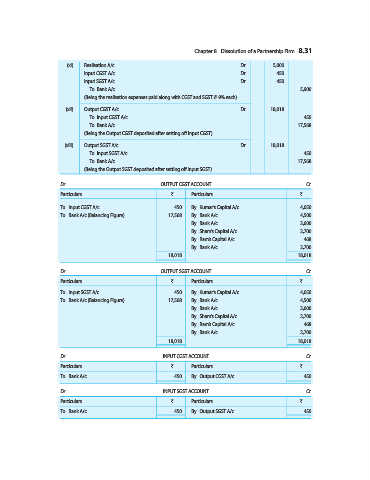

(xi) Realisation A/c ...Dr. 5,000

Input CGST A/c ...Dr. 450

Input SGST A/c ...Dr. 450

To Bank A/c 5,900

(Being the realisation expenses paid along with CGST and SGST @ 9% each)

(xii) Output CGST A/c ...Dr. 18,018

To Input CGST A/c 450

To Bank A/c 17,568

(Being the Output CGST deposited after setting off Input CGST)

(xiii) Output SGST A/c ...Dr. 18,018

To Input SGST A/c 450

To Bank A/c 17,568

(Being the Output SGST deposited after setting off Input SGST)

Dr. OUTPUT CGST ACCOUNT Cr.

Particulars ` Particulars `

To Input CGST A/c 450 By Kumar’s Capital A/c 4,050

To Bank A/c (Balancing Figure) 17,568 By Bank A/c 4,500

By Bank A/c 3,600

By Sham’s Capital A/c 2,700

By Ram’s Capital A/c 468

By Bank A/c 2,700

18,018 18,018

Dr. OUTPUT SGST ACCOUNT Cr.

Particulars ` Particulars `

To Input SGST A/c 450 By Kumar’s Capital A/c 4,050

To Bank A/c (Balancing Figure) 17,568 By Bank A/c 4,500

By Bank A/c 3,600

By Sham’s Capital A/c 2,700

By Ram’s Capital A/c 468

By Bank A/c 2,700

18,018 18,018

Dr. INPUT CGST ACCOUNT Cr.

Particulars ` Particulars `

To Bank A/c 450 By Output CGST A/c 450

Dr. INPUT SGST ACCOUNT Cr.

Particulars ` Particulars `

To Bank A/c 450 By Output SGST A/c 450