Page 23 - DEBKVOL-1

P. 23

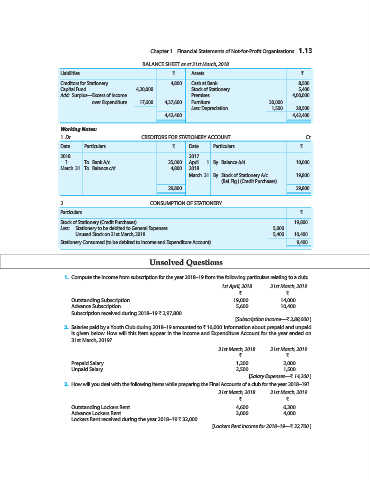

Chapter 1 Financial Statements of Not-for-Profit Organisations 1.13

.

BALANCE SHEET as at 31st March, 2018

Liabilities ` Assets `

Creditors for Stationery 4,800 Cash at Bank 8,500

Capital Fund 4,20,000 Stock of Stationery 5,400

Add: Surplus—Excess of Income Premises 4,00,000

over Expenditure 17,600 4,37,600 Furniture 30,000

Less: Depreciation 1,500 28,500

4,42,400 4,42,400

Working Notes:

1. Dr. CREDITORS FOR STATIONERY ACCOUNT Cr.

Date Particulars ` Date Particulars `

2018 2017

? To Bank A/c 25,000 April 1 By Balance b/d 10,000

March 31 To Balance c/d 4,800 2018

March 31 By Stock of Stationery A/c 19,800

(Bal. Fig.) (Credit Purchases)

29,800 29,800

2. CONSUMPTION OF STATIONERY

Particulars `

Stock of Stationery (Credit Purchases) 19,800

Less: Stationery to be debited to General Expenses 5,000

Unused Stock on 31st March, 2018 5,400 10,400

Stationery Consumed (to be debited to Income and Expenditure Account) 9,400

Unsolved Questions

1. Compute the income from subscription for the year 2018–19 from the following particulars relating to a club:

1st April, 2018 31st March, 2019

` `

Outstanding Subscription 19,000 14,000

Advance Subscription 5,600 10,400

Subscription received during 2018–19 ` 2,97,800.

[Subscription Income—` 2,88,000.]

2. Salaries paid by a Youth Club during 2018–19 amounted to ` 16,000. Information about prepaid and unpaid

is given below. How will this item appear in the Income and Expenditure Account for the year ended on

31st March, 2019?

31st March, 2018 31st March, 2019

` `

Prepaid Salary 1,200 2,000

Unpaid Salary 2,500 1,500

[Salary Expenses—` 14,200.]

3. How will you deal with the following items while preparing the Final Accounts of a club for the year 2018–19?

31st March, 2018 31st March, 2019

` `

Outstanding Lockers Rent 4,600 6,300

Advance Lockers Rent 3,000 4,000

Lockers Rent received during the year 2018–19 ` 32,000.

[Lockers Rent Income for 2018–19—` 32,700.]