Page 52 - DEBKVOL-1

P. 52

2.24 Double Entry Book Keeping—CBSE XII

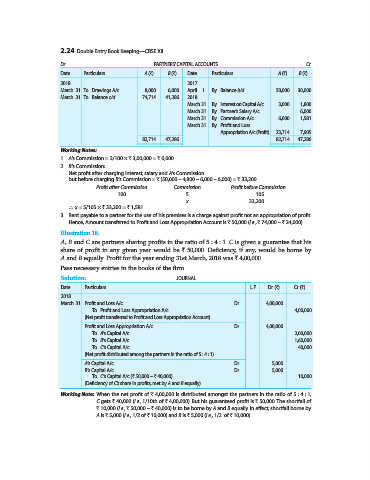

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Date Particulars A (`) B (`) Date Particulars A (`) B (`)

2018 2017

March 31 To Drawings A/c 8,000 6,000 April 1 By Balance b/d 50,000 30,000

March 31 To Balance c/d 74,714 41,286 2018

March 31 By Interest on Capital A/c 3,000 1,800

March 31 By Partner’s Salary A/c ... 6,000

March 31 By Commission A/c 6,000 1,581

March 31 By Profit and Loss

Appropriation A/c (Profit) 23,714 7,905

82,714 47,286 82,714 47,286

Working Notes:

1. A’s Commission = 2/100 × ` 3,00,000 = ` 6,000

2. B’s Commission:

Net profit after charging interest, salary and A’s Commission

but before charging B’s Commission = ` (50,000 – 4,800 – 6,000 – 6,000) = ` 33,200

Profit after Commission Commission Profit before Commission

100 5 105

x 33,200

∴ x = 5/105 × ` 33,200 = ` 1,581.

3. Rent payable to a partner for the use of his premises is a charge against profit not an appropriation of profit.

Hence, Amount transferred to Profit and Loss Appropriation Account is ` 50,000 (i.e., ` 74,000 – ` 24,000).

Illustration 18.

A, B and C are partners sharing profits in the ratio of 5 : 4 : 1. C is given a guarantee that his

share of profit in any given year would be ` 50,000. Deficiency, if any, would be borne by

A and B equally. Profit for the year ending 31st March, 2018 was ` 4,00,000.

Pass necessary entries in the books of the firm.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2018

March 31 Profit and Loss A/c ...Dr. 4,00,000

To Profit and Loss Appropriation A/c 4,00,000

(Net profit transferred to Profit and Loss Appropriation Account)

Profit and Loss Appropriation A/c ...Dr. 4,00,000

To A’s Capital A/c 2,00,000

To B’s Capital A/c 1,60,000

To C’s Capital A/c 40,000

(Net profit distributed among the partners in the ratio of 5 : 4 : 1)

A’s Capital A/c ...Dr. 5,000

B’s Capital A/c ...Dr. 5,000

To C’s Capital A/c (` 50,000 – ` 40,000) 10,000

(Deficiency of C’s share in profits, met by A and B equally)

Working Note: When the net profit of ` 4,00,000 is distributed amongst the partners in the ratio of 5 : 4 : 1,

C gets ` 40,000 (i.e., 1/10th of ` 4,00,000). But his guaranteed profit is ` 50,000. The shortfall of

` 10,000 (i.e., ` 50,000 – ` 40,000) is to be borne by A and B equally. In effect, shortfall borne by

A is ` 5,000 (i.e., 1/2 of ` 10,000) and B is ` 5,000 (i.e., 1/2 of ` 10,000).