Page 49 - DEBKVOL-1

P. 49

Chapter 2 Accounting for Partnership Firms—Fundamentals 2.21

.

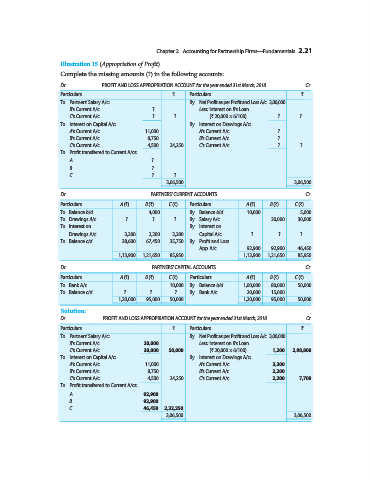

Illustration 15 (Appropriation of Profit).

Complete the missing amounts (?) in the following accounts:

Dr. PROFIT AND LOSS APPROPRIATION ACCOUNT for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Partners’ Salary A/c: By Net Profit as per Profit and Loss A/c 3,00,000

B’s Current A/c ? Less: Interest on B’s Loan

C’s Current A/c ? ? (` 20,000 × 6/100) ? ?

To Interest on Capital A/c: By Interest on Drawings A/c:

A’s Current A/c 11,000 A’s Current A/c ?

B’s Current A/c 8,750 B’s Current A/c ?

C’s Current A/c 4,500 24,250 C’s Current A/c ? ?

To Profit transferred to Current A/cs:

A ?

B ?

C ? ?

3,06,500 3,06,500

Dr. PARTNERS’ CURRENT ACCOUNTS Cr.

Particulars A (`) B (`) C (`) Particulars A (`) B (`) C (`)

To Balance b/d 4,000 By Balance b/d 10,000 5,000

To Drawings A/c ? ? ? By Salary A/c 20,000 30,000

To Interest on By Interest on

Drawings A/c 3,300 2,200 2,200 Capital A/c ? ? ?

To Balance c/d 38,600 67,450 35,750 By Profit and Loss

App. A/c 92,900 92,900 46,450

1,13,900 1,21,650 85,950 1,13,900 1,21,650 85,950

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars A (`) B (`) C (`) Particulars A (`) B (`) C (`)

To Bank A/c 10,000 By Balance b/d 1,00,000 80,000 50,000

To Balance c/d ? ? ? By Bank A/c 20,000 15,000

1,20,000 95,000 50,000 1,20,000 95,000 50,000

Solution:

Dr. PROFIT AND LOSS APPROPRIATION ACCOUNT for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Partners’ Salary A/c: By Net Profit as per Profit and Loss A/c 3,00,000

B’s Current A/c 20,000 Less: Interest on B’s Loan

C’s Current A/c 30,000 50,000 (` 20,000 × 6/100) 1,200 2,98,800

To Interest on Capital A/c: By Interest on Drawings A/c:

A’s Current A/c 11,000 A’s Current A/c 3,300

B’s Current A/c 8,750 B’s Current A/c 2,200

C’s Current A/c 4,500 24,250 C’s Current A/c 2,200 7,700

To Profit transferred to Current A/cs:

A 92,900

B 92,900

C 46,450 2,32,250

3,06,500 3,06,500