Page 48 - DEBKVOL-1

P. 48

2.20 Double Entry Book Keeping—CBSE XII

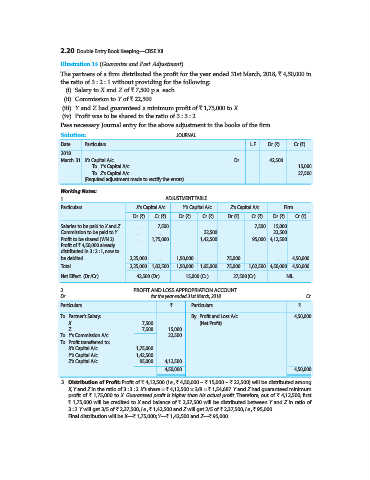

Illustration 14 (Guarantee and Past Adjustment).

The partners of a firm distributed the profit for the year ended 31st March, 2018, ` 4,50,000 in

the ratio of 3 : 2 : 1 without providing for the following:

(i) Salary to X and Z of ` 7,500 p.a. each.

(ii) Commission to Y of ` 22,500.

(iii) Y and Z had guaranteed a minimum profit of ` 1,75,000 to X.

(iv) Profit was to be shared in the ratio of 3 : 3 : 2.

Pass necessary Journal entry for the above adjustment in the books of the firm.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2018

March 31 X’s Capital A/c ...Dr. 42,500

To Y’s Capital A/c 15,000

To Z’s Capital A/c 27,500

(Required adjustment made to rectify the errors)

Working Notes:

1. ADJUSTMENT TABLE

Particulars X’s Capital A/c Y’s Capital A/c Z’s Capital A/c Firm

Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`)

Salaries to be paid to X and Z ... 7,500 ... ... ... 7,500 15,000 ...

Commission to be paid to Y ... ... ... 22,500 ... ... 22,500 ...

Profit to be shared (WN 2) ... 1,75,000 ... 1,42,500 ... 95,000 4,12,500 ...

Profit of ` 4,50,000 already

distributed in 3 : 2 : 1, now to

be debited 2,25,000 ... 1,50,000 ... 75,000 ... ... 4,50,000

Total 2,25,000 1,82,500 1,50,000 1,65,000 75,000 1,02,500 4,50,000 4,50,000

Net Effect (Dr./Cr.) 42,500 (Dr.) 15,000 (Cr.) 27,500 (Cr.) NIL

2. PROFIT AND LOSS APPROPRIATION ACCOUNT

Dr. for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Partner’s Salary: By Profit and Loss A/c 4,50,000

X 7,500 (Net Profit)

Z 7,500 15,000

To Y’s Commission A/c 22,500

To Profit transferred to:

X’s Capital A/c 1,75,000

Y’s Capital A/c 1,42,500

Z’s Capital A/c 95,000 4,12,500

4,50,000 4,50,000

3. Distribution of Profit: Profit of ` 4,12,500 (i.e., ` 4,50,000 – ` 15,000 – ` 22,500) will be distributed among

X, Y and Z in the ratio of 3 : 3 : 2. X’s share = ` 4,12,500 × 3/8 = ` 1,54,687. Y and Z had guaranteed minimum

profit of ` 1,75,000 to X. Guaranteed profit is higher than his actual profit. Therefore, out of ` 4,12,500, first

` 1,75,000 will be credited to X and balance of ` 2,37,500 will be distributed between Y and Z in ratio of

3 : 2. Y will get 3/5 of ` 2,37,500, i.e., ` 1,42,500 and Z will get 2/5 of ` 2,37,500, i.e., ` 95,000.

Final distribution will be X—` 1,75,000; Y—` 1,42,500 and Z—` 95,000.