Page 47 - DEBKVOL-1

P. 47

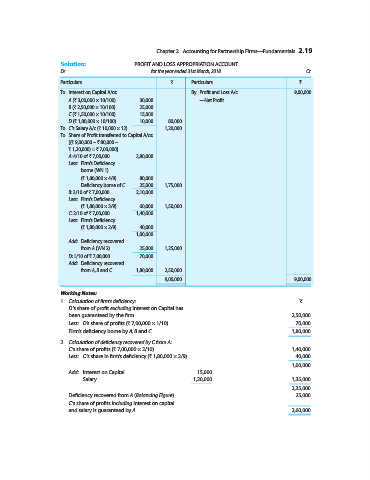

Chapter 2 Accounting for Partnership Firms—Fundamentals 2.19

.

Solution: PROFIT AND LOSS APPROPRIATION ACCOUNT

Dr. for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Interest on Capital A/cs: By Profit and Loss A/c 9,00,000

A (` 3,00,000 × 10/100) 30,000 —Net Profit

B (` 2,50,000 × 10/100) 25,000

C (` 1,50,000 × 10/100) 15,000

D (` 1,00,000 × 10/100) 10,000 80,000

To C’s Salary A/c (` 10,000 × 12) 1,20,000

To Share of Profit transferred to Capital A/cs:

[(` 9,00,000 – ` 80,000 –

` 1,20,000) = ` 7,00,000]

A: 4/10 of ` 7,00,000 2,80,000

Less: Firm’s Deficiency

borne (WN 1)

(` 1,80,000 × 4/9) 80,000

Deficiency borne of C 25,000 1,75,000

B: 3/10 of ` 7,00,000 2,10,000

Less: Firm’s Deficiency

(` 1,80,000 × 3/9) 60,000 1,50,000

C: 2/10 of ` 7,00,000 1,40,000

Less: Firm’s Deficiency

(` 1,80,000 × 2/9) 40,000

1,00,000

Add: Deficiency recovered

from A (WN 2) 25,000 1,25,000

D: 1/10 of ` 7,00,000 70,000

Add: Deficiency recovered

from A, B and C 1,80,000 2,50,000

9,00,000 9,00,000

Working Notes:

1. Calculation of firm’s deficiency: `

D’s share of profit excluding interest on Capital has

been guaranteed by the firm 2,50,000

Less: D’s share of profits (` 7,00,000 × 1/10) 70,000

Firm’s deficiency borne by A, B and C 1,80,000

2. Calculation of deficiency recovered by C from A:

C’s share of profits (` 7,00,000 × 2/10) 1,40,000

Less: C’s share in firm’s deficiency (` 1,80,000 × 2/9) 40,000

1,00,000

Add: Interest on Capital 15,000

Salary 1,20,000 1,35,000

2,35,000

Deficiency recovered from A (Balancing Figure) 25,000

C’s share of profits including interest on capital

and salary is guaranteed by A 2,60,000