Page 51 - DEBKVOL-1

P. 51

Chapter 2 Accounting for Partnership Firms—Fundamentals 2.23

.

Redrawn Profit and Loss Appropriation Account is as follows:

Dr. PROFIT AND LOSS APPROPRIATION ACCOUNT for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Profit transferred to Capital A/cs: By Profit and Loss A/c (Net Profit) 2,82,000

Amit (1/2) 1,41,000 (After interest on loan)

Bishan (1/2) 1,41,000 2,82,000 (` 2,94,000 – ` 12,000)

2,82,000 2,82,000

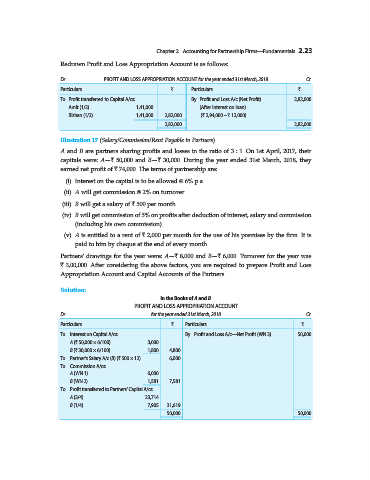

Illustration 17 (Salary/Commission/Rent Payable to Partners).

A and B are partners sharing profits and losses in the ratio of 3 : 1. On 1st April, 2017, their

capitals were: A—` 50,000 and B—` 30,000. During the year ended 31st March, 2018, they

earned net profit of ` 74,000. The terms of partnership are:

(i) Interest on the capital is to be allowed @ 6% p.a.

(ii) A will get commission @ 2% on turnover.

(iii) B will get a salary of ` 500 per month.

(iv) B will get commission of 5% on profits after deduction of interest, salary and commission

(including his own commission).

(v) A is entitled to a rent of ` 2,000 per month for the use of his premises by the firm. It is

paid to him by cheque at the end of every month.

Partners’ drawings for the year were: A—` 8,000 and B—` 6,000. Turnover for the year was

` 3,00,000. After considering the above factors, you are required to prepare Profit and Loss

Appropriation Account and Capital Accounts of the Partners.

Solution:

In the Books of A and B

PROFIT AND LOSS APPROPRIATION ACCOUNT

Dr. for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Interest on Capital A/cs: By Profit and Loss A/c—Net Profit (WN 3) 50,000

A (` 50,000 × 6/100) 3,000

B (` 30,000 × 6/100) 1,800 4,800

To Partner’s Salary A/c (B) (` 500 × 12) 6,000

To Commission A/cs:

A (WN 1) 6,000

B (WN 2) 1,581 7,581

To Profit transferred to Partners’ Capital A/cs:

A (3/4) 23,714

B (1/4) 7,905 31,619

50,000 50,000