Page 74 - DEBKVOL-1

P. 74

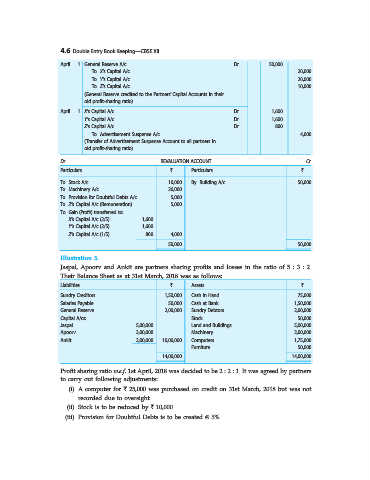

4.6 Double Entry Book Keeping—CBSE XII

April 1 General Reserve A/c ...Dr. 50,000

To X’s Capital A/c 20,000

To Y’s Capital A/c 20,000

To Z’s Capital A/c 10,000

(General Reserve credited to the Partners’ Capital Accounts in their

old profit-sharing ratio)

April 1 X’s Capital A/c ...Dr. 1,600

Y’s Capital A/c ...Dr. 1,600

Z’s Capital A/c ...Dr. 800

To Advertisement Suspense A/c 4,000

(Transfer of Advertisement Suspense Account to all partners in

old profit-sharing ratio)

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Stock A/c 10,000 By Building A/c 50,000

To Machinery A/c 26,000

To Provision for Doubtful Debts A/c 5,000

To Z’s Capital A/c (Remuneration) 5,000

To Gain (Profit) transferred to:

X’s Capital A/c (2/5) 1,600

Y’s Capital A/c (2/5) 1,600

Z’s Capital A/c (1/5) 800 4,000

50,000 50,000

Illustration 3.

Jaspal, Apoorv and Ankit are partners sharing profits and losses in the ratio of 5 : 3 : 2.

Their Balance Sheet as at 31st March, 2018 was as follows:

Liabilities ` Assets `

Sundry Creditors 1,50,000 Cash in Hand 75,000

Salaries Payable 50,000 Cash at Bank 1,50,000

General Reserve 2,00,000 Sundry Debtors 2,00,000

Capital A/cs: Stock 50,000

Jaspal 5,00,000 Land and Buildings 5,00,000

Apoorv 3,00,000 Machinery 2,00,000

Ankit 2,00,000 10,00,000 Computers 1,75,000

Furniture 50,000

14,00,000 14,00,000

Profit sharing ratio w.e.f. 1st April, 2018 was decided to be 2 : 2 : 1. It was agreed by partners

to carry out following adjustments:

(i) A computer for ` 25,000 was purchased on credit on 31st March, 2018 but was not

recorded due to oversight.

(ii) Stock is to be reduced by ` 10,000.

(iii) Provision for Doubtful Debts is to be created @ 5%.