Page 76 - DEBKVOL-1

P. 76

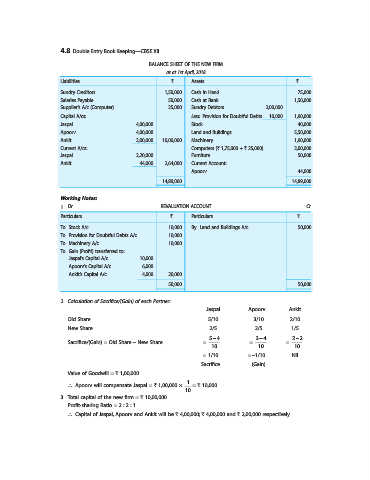

4.8 Double Entry Book Keeping—CBSE XII

BALANCE SHEET OF THE NEW FIRM

as at 1st April, 2018

Liabilities ` Assets `

Sundry Creditors 1,50,000 Cash in Hand 75,000

Salaries Payable 50,000 Cash at Bank 1,50,000

Supplier’s A/c (Computer) 25,000 Sundry Debtors 2,00,000

Capital A/cs: Less: Provision for Doubtful Debts 10,000 1,90,000

Jaspal 4,00,000 Stock 40,000

Apoorv 4,00,000 Land and Buildings 5,50,000

Ankit 2,00,000 10,00,000 Machinery 1,90,000

Current A/cs: Computers (` 1,75,000 + ` 25,000) 2,00,000

Jaspal 2,20,000 Furniture 50,000

Ankit 44,000 2,64,000 Current Account:

Apoorv 44,000

14,89,000 14,89,000

Working Notes:

1. Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Stock A/c 10,000 By Land and Buildings A/c 50,000

To Provision for Doubtful Debts A/c 10,000

To Machinery A/c 10,000

To Gain (Profit) transferred to:

Jaspal’s Capital A/c 10,000

Apoorv’s Capital A/c 6,000

Ankit’s Capital A/c 4,000 20,000

50,000 50,000

2. Calculation of Sacrifice/(Gain) of each Partner:

Jaspal Apoorv Ankit

Old Share 5/10 3/10 2/10

New Share 2/5 2/5 1/5

54- 34- 2 2-

Sacrifice/(Gain) = Old Share – New Share = = =

10 10 10

= 1/10 = –1/10 Nil

Sacrifice (Gain)

Value of Goodwill = ` 1,00,000

1

∴ Apoorv will compensate Jaspal = ` 1,00,000 × = ` 10,000.

10

3. Total capital of the new firm = ` 10,00,000

Profit-sharing Ratio = 2 : 2 : 1

∴ Capital of Jaspal, Apoorv and Ankit will be ` 4,00,000; ` 4,00,000 and ` 2,00,000 respectively.