Page 75 - DEBKVOL-1

P. 75

Chapter 4 Change in Profit-Sharing Ratio Among the Existing Partners 4.7

.

(iv) Land and Buildings to be appreciated by 10% and Machinery to be reduced by 5%.

(v) Goodwill of the firm is valued at ` 1,00,000.

(vi) Total capital of the firm was to be ` 10,00,000 and is to be in their profit-sharing ratio.

Excess or short capital is to be adjusted through their Current Accounts.

Pass the Journal entries and prepare Balance Sheet of the new firm.

Solution: JOURNAL

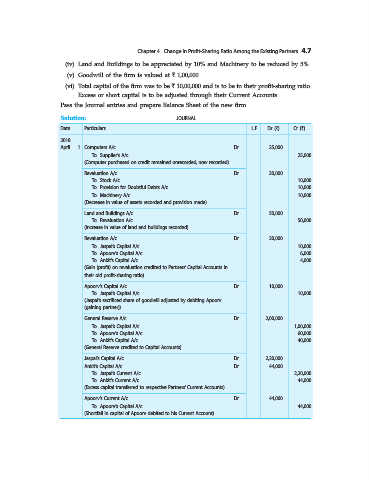

Date Particulars L.F. Dr. (`) Cr. (`)

2018

April 1 Computers A/c ...Dr. 25,000

To Supplier’s A/c 25,000

(Computer purchased on credit remained unrecorded, now recorded)

Revaluation A/c ...Dr. 30,000

To Stock A/c 10,000

To Provision for Doubtful Debts A/c 10,000

To Machinery A/c 10,000

(Decrease in value of assets recorded and provision made)

Land and Buildings A/c ...Dr. 50,000

To Revaluation A/c 50,000

(Increase in value of land and buildings recorded)

Revaluation A/c ...Dr. 20,000

To Jaspal’s Capital A/c 10,000

To Apoorv’s Capital A/c 6,000

To Ankit’s Capital A/c 4,000

(Gain (profit) on revaluation credited to Partners’ Capital Accounts in

their old profit-sharing ratio)

Apoorv’s Capital A/c ...Dr. 10,000

To Jaspal’s Capital A/c 10,000

(Jaspal’s sacrificed share of goodwill adjusted by debiting Apoorv

(gaining partner))

General Reserve A/c ...Dr. 2,00,000

To Jaspal’s Capital A/c 1,00,000

To Apoorv’s Capital A/c 60,000

To Ankit’s Capital A/c 40,000

(General Reserve credited to Capital Accounts)

Jaspal’s Capital A/c ...Dr. 2,20,000

Ankit’s Capital A/c ...Dr. 44,000

To Jaspal’s Current A/c 2,20,000

To Ankit’s Current A/c 44,000

(Excess capital transferred to respective Partners’ Current Accounts)

Apoorv’s Current A/c ...Dr. 44,000

To Apoorv’s Capital A/c 44,000

(Shortfall in capital of Apoorv debited to his Current Account)