Page 83 - DEBKVOL-1

P. 83

Chapter 4 Change in Profit-Sharing Ratio Among the Existing Partners 4.15

.

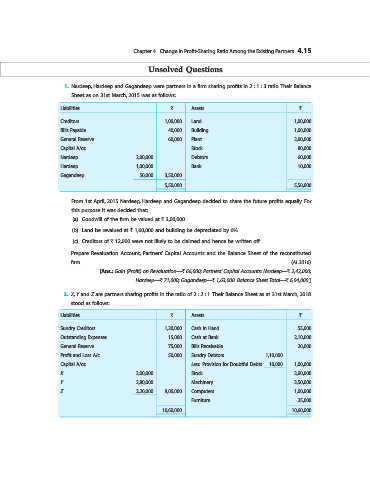

Unsolved Questions

1. Nardeep, Hardeep and Gagandeep were partners in a firm sharing profits in 2 : 1 : 3 ratio. Their Balance

Sheet as on 31st March, 2015 was as follows:

Liabilities ` Assets `

Creditors 1,00,000 Land 1,00,000

Bills Payable 40,000 Building 1,00,000

General Reserve 60,000 Plant 2,00,000

Capital A/cs: Stock 80,000

Nardeep 2,00,000 Debtors 60,000

Hardeep 1,00,000 Bank 10,000

Gagandeep 50,000 3,50,000

5,50,000 5,50,000

From 1st April, 2015 Nardeep, Hardeep and Gagandeep decided to share the future profits equally. For

this purpose it was decided that:

(a) Goodwill of the firm be valued at ` 3,00,000.

(b) Land be revalued at ` 1,60,000 and building be depreciated by 6%.

(c) Creditors of ` 12,000 were not likely to be claimed and hence be written off.

Prepare Revaluation Account, Partners’ Capital Accounts and the Balance Sheet of the reconstituted

firm. (AI 2016)

[Ans.: Gain (Profit) on Revaluation—` 66,000; Partners’ Capital Accounts: Nardeep—` 2,42,000;

Hardeep—` 71,000; Gagandeep—` 1,63,000. Balance Sheet Total—` 6,04,000.]

2. X, Y and Z are partners sharing profits in the ratio of 2 : 2 : 1. Their Balance Sheet as at 31st March, 2018

stood as follows:

Liabilities ` Assets `

Sundry Creditors 1,20,000 Cash in Hand 55,000

Outstanding Expenses 15,000 Cash at Bank 2,10,000

General Reserve 75,000 Bills Receivable 20,000

Profit and Loss A/c 50,000 Sundry Debtors 1,10,000

Capital A/cs: Less: Provision for Doubtful Debts 10,000 1,00,000

X 3,00,000 Stock 2,00,000

Y 2,80,000 Machinery 3,50,000

Z 2,20,000 8,00,000 Computers 1,00,000

Furniture 25,000

10,60,000 10,60,000