Page 80 - DEBKVOL-1

P. 80

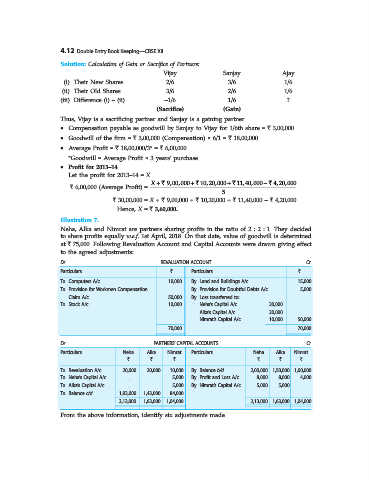

4.12 Double Entry Book Keeping—CBSE XII

Solution: Calculation of Gain or Sacrifice of Partners:

Vijay Sanjay Ajay

(i) Their New Shares 2/6 3/6 1/6

(ii) Their Old Shares 3/6 2/6 1/6

(iii) Difference (i) – (ii) –1/6 1/6 ?

(Sacrifice) (Gain)

Thus, Vijay is a sacrificing partner and Sanjay is a gaining partner.

• Compensation payable as goodwill by Sanjay to Vijay for 1/6th share = ` 3,00,000.

• Goodwill of the firm = ` 3,00,000 (Compensation) × 6/1 = ` 18,00,000.

• Average Profit = ` 18,00,000/3* = ` 6,00,000

*Goodwill = Average Profit × 3 years’ purchase.

• Profit for 2013–14

Let the profit for 2013–14 = X

X + ` 9,00,000 + ` 10,20,000 + ` 11,40,000 - ` 4,20,000

` 6,00,000 (Average Profit) =

5

` 30,00,000 = X + ` 9,00,000 + ` 10,20,000 + ` 11,40,000 – ` 4,20,000

Hence, X = ` 3,60,000.

Illustration 7.

Neha, Alka and Nimrat are partners sharing profits in the ratio of 2 : 2 : 1. They decided

to share profits equally w.e.f. 1st April, 2018. On that date, value of goodwill is determined

at ` 75,000. Following Revaluation Account and Capital Accounts were drawn giving effect

to the agreed adjustments:

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Computers A/c 10,000 By Land and Buildings A/c 15,000

To Provision for Workmen Compensation By Provision for Doubtful Debts A/c 5,000

Claim A/c 50,000 By Loss transferred to:

To Stock A/c 10,000 Neha’s Capital A/c 20,000

Alka’s Capital A/c 20,000

Nimrat’s Capital A/c 10,000 50,000

70,000 70,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Neha Alka Nimrat Particulars Neha Alka Nimrat

` ` ` ` ` `

To Revaluation A/c 20,000 20,000 10,000 By Balance b/d 2,00,000 1,50,000 1,00,000

To Neha’s Capital A/c ... ... 5,000 By Profit and Loss A/c 8,000 8,000 4,000

To Alka’s Capital A/c ... ... 5,000 By Nimrat’s Capital A/c 5,000 5,000 ...

To Balance c/d 1,93,000 1,43,000 84,000

2,13,000 1,63,000 1,04,000 2,13,000 1,63,000 1,04,000

From the above information, identify six adjustments made.