Page 79 - DEBKVOL-1

P. 79

Chapter 4 Change in Profit-Sharing Ratio Among the Existing Partners 4.11

.

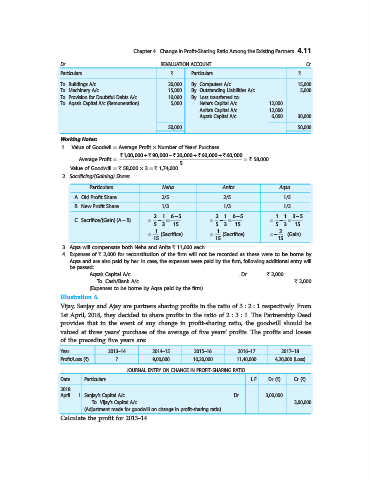

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Buildings A/c 20,000 By Computers A/c 15,000

To Machinery A/c 15,000 By Outstanding Liabilities A/c 5,000

To Provision for Doubtful Debts A/c 10,000 By Loss transferred to:

To Aqsa’s Capital A/c (Remuneration) 5,000 Neha’s Capital A/c 12,000

Anita’s Capital A/c 12,000

Aqsa’s Capital A/c 6,000 30,000

50,000 50,000

Working Notes:

1. Value of Goodwil = Average Profit × Number of Years’ Purchase

` 1,00,000 + ` 90,000 – 20,000 +` ` 60,000 + ` 60,000

Average Profit = = ` 58,000

5

Value of Goodwill = ` 58,000 × 3 = ` 1,74,000.

2. Sacrificing/(Gaining) Share:

Particulars Neha Anita Aqsa

A. Old Profit Share 2/5 2/5 1/5

B. New Profit Share 1/3 1/3 1/3

2 1 65- 2 1 65- 1 1 35-

C. Sacrifice/(Gain) (A – B) = - = = - = = - =

5 3 15 5 3 15 5 3 15

1 1 2

= (Sacrifice) = (Sacrifice) = - (Gain)

15 15 15

3. Aqsa will compensate both Neha and Anita ` 11,600 each.

4. Expenses of ` 2,000 for reconstitution of the firm will not be recorded as these were to be borne by

Aqsa and are also paid by her. In case, the expenses were paid by the firm, following additional entry will

be passed:

Aqsa’s Capital A/c ...Dr. ` 2,000

To Cash/Bank A/c ` 2,000

(Expenses to be borne by Aqsa paid by the firm)

Illustration 6.

Vijay, Sanjay and Ajay are partners sharing profits in the ratio of 3 : 2 : 1 respectively. From

1st April, 2018, they decided to share profits in the ratio of 2 : 3 : 1. The Partnership Deed

provides that in the event of any change in profit-sharing ratio, the goodwill should be

valued at three years’ purchase of the average of five years’ profits. The profits and losses

of the preceding five years are:

Year 2013–14 2014–15 2015–16 2016–17 2017–18

Profit/Loss (`) ? 9,00,000 10,20,000 11,40,000 4,20,000 (Loss)

JOURNAL ENTRY ON CHANGE IN PROFIT-SHARING RATIO

Date Particulars L.F. Dr. (`) Cr. (`)

2018

April 1 Sanjay’s Capital A/c ...Dr. 3,00,000

To Vijay’s Capital A/c 3,00,000

(Adjustment made for goodwill on change in profit-sharing ratio)

Calculate the profit for 2013–14.