Page 101 - DEBKVOL-1

P. 101

Chapter 5 Admission of a Partner 5.17

.

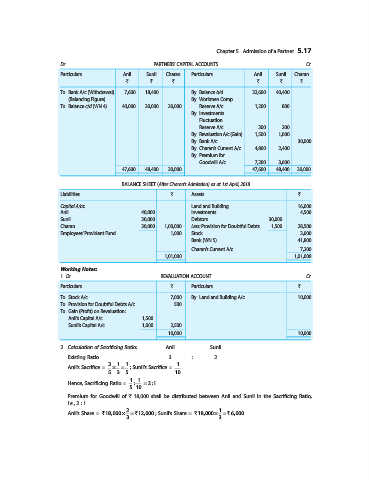

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Anil Sunil Charan Particulars Anil Sunil Charan

` ` ` ` ` `

To Bank A/c (Withdrawal) 7,600 18,400 ... By Balance b/d 32,600 40,400 ...

(Balancing Figure) By Workmen Comp.

To Balance c/d (WN 4) 40,000 30,000 30,000 Reserve A/c 1,200 800 ...

By Investments

Fluctuation

Reserve A/c 300 200 ...

By Revaluation A/c (Gain) 1,500 1,000 ...

By Bank A/c ... ... 30,000

By Charan’s Current A/c 4,800 2,400 ...

By Premium for

Goodwill A/c 7,200 3,600 ...

47,600 48,400 30,000 47,600 48,400 30,000

BALANCE SHEET (After Charan’s Admission) as at 1st April, 2018

Liabilities ` Assets `

Capital A/cs: Land and Building 16,000

Anil 40,000 Investments 4,500

Sunil 30,000 Debtors 30,000

Charan 30,000 1,00,000 Less: Provision for Doubtful Debts 1,500 28,500

Employees’ Provident Fund 1,000 Stock 3,000

Bank (WN 5) 41,800

Charan’s Current A/c 7,200

1,01,000 1,01,000

Working Notes:

1. Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Stock A/c 7,000 By Land and Building A/c 10,000

To Provision for Doubtful Debts A/c 500

To Gain (Profit) on Revaluation:

Anil’s Capital A/c 1,500

Sunil’s Capital A/c 1,000 2,500

10,000 10,000

2. Calculation of Sacrificing Ratio: Anil Sunil

Existing Ratio 3 : 2

3 1 1 1

Anil’s Sacrifice = ¥ = ; Sunil’s Sacrifice =

5 3 5 10

11

Hence, Sacrificing Ratio = : = 2 :1

5 10

Premium for Goodwill of ` 18,000 shall be distributed between Anil and Sunil in the Sacrificing Ratio,

i.e., 2 : 1

2 1

Anil’s Share = `18,000 ¥ = `12,000 ; Sunil’s Share = `18,000 ¥ = ` 6,000.

3 3