Page 128 - DEBKVOL-1

P. 128

5.44 Double Entry Book Keeping—CBSE XII

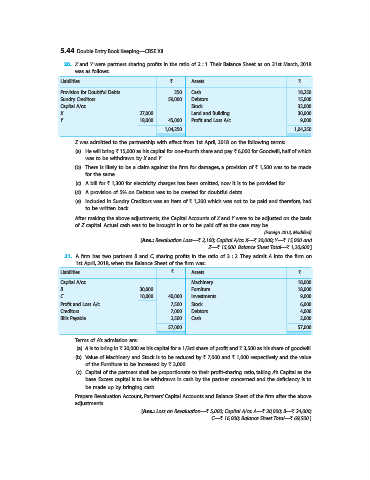

20. X and Y were partners sharing profits in the ratio of 2 : 1. Their Balance Sheet as on 31st March, 2018

was as follows:

Liabilities ` Assets `

Provision for Doubtful Debts 250 Cash 18,250

Sundry Creditors 59,000 Debtors 15,000

Capital A/cs: Stock 32,000

X 27,000 Land and Building 30,000

Y 18,000 45,000 Profit and Loss A/c 9,000

1,04,250 1,04,250

Z was admitted to the partnership with effect from 1st April, 2018 on the following terms:

(a) He will bring ` 15,000 as his capital for one-fourth share and pay ` 6,000 for Goodwill, half of which

was to be withdrawn by X and Y.

(b) There is likely to be a claim against the firm for damages, a provision of ` 1,500 was to be made

for the same.

(c) A bill for ` 1,300 for electricity charges has been omitted, now it is to be provided for.

(d) A provision of 5% on Debtors was to be created for doubtful debts.

(e) Included in Sundry Creditors was an item of ` 1,200 which was not to be paid and therefore, had

to be written back.

After making the above adjustments, the Capital Accounts of X and Y were to be adjusted on the basis

of Z capital. Actual cash was to be brought in or to be paid off as the case may be.

(Foreign 2012, Modified)

[Ans.: Revaluation Loss—` 2,100; Capital A/cs: X—` 30,000; Y—` 15,000 and

Z—` 15,000. Balance Sheet Total—` 1,20,600.]

21. A firm has two partners B and C, sharing profits in the ratio of 3 : 2. They admit A into the firm on

1st April, 2018, when the Balance Sheet of the firm was:

Liabilities ` Assets `

Capital A/cs: Machinery 18,000

B 30,000 Furniture 18,000

C 10,000 40,000 Investments 9,000

Profit and Loss A/c 7,500 Stock 6,000

Creditors 7,000 Debtors 4,000

Bills Payable 2,500 Cash 2,000

57,000 57,000

Terms of A’s admission are:

(a) A is to bring in ` 20,000 as his capital for a 1/3rd share of profit and ` 3,500 as his share of goodwill.

(b) Value of Machinery and Stock is to be reduced by ` 7,000 and ` 1,000 respectively and the value

of the Furniture to be increased by ` 3,000.

(c) Capital of the partners shall be proportionate to their profit-sharing ratio, taking A’s Capital as the

base. Excess capital is to be withdrawn in cash by the partner concerned and the deficiency is to

be made up by bringing cash.

Prepare Revaluation Account, Partners’ Capital Accounts and Balance Sheet of the firm after the above

adjustments.

[Ans.: Loss on Revaluation—` 5,000; Capital A/cs: A—` 20,000; B—` 24,000;

C—` 16,000; Balance Sheet Total—` 69,500.]