Page 129 - DEBKVOL-1

P. 129

Chapter 5 Admission of a Partner 5.45

.

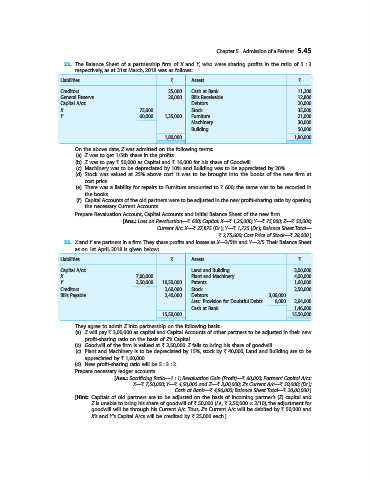

22. The Balance Sheet of a partnership firm of X and Y, who were sharing profits in the ratio of 5 : 3

respectively, as at 31st March, 2018 was as follows:

Liabilities ` Assets `

Creditors 25,000 Cash at Bank 11,200

General Reserve 20,000 Bills Receivable 12,800

Capital A/cs: Debtors 20,000

X 75,000 Stock 35,000

Y 60,000 1,35,000 Furniture 21,000

Machinery 30,000

Building 50,000

1,80,000 1,80,000

On the above date, Z was admitted on the following terms:

(a) Z was to get 1/5th share in the profits.

(b) Z was to pay ` 50,000 as Capital and ` 16,000 for his share of Goodwill.

(c) Machinery was to be depreciated by 10% and Building was to be appreciated by 20%.

(d) Stock was valued at 25% above cost. It was to be brought into the books of the new firm at

cost price.

(e) There was a liability for repairs to Furniture amounted to ` 600; the same was to be recorded in

the books.

(f) Capital Accounts of the old partners were to be adjusted in the new profit-sharing ratio by opening

the necessary Current Accounts.

Prepare Revaluation Account, Capital Accounts and initial Balance Sheet of the new firm.

[Ans.: Loss on Revaluation—` 600; Capital: X—` 1,25,000; Y—` 75,000; Z—` 50,000;

Current A/c: X—` 27,875 (Dr.); Y—` 1,725 (Dr.); Balance Sheet Total—

` 2,75,600; Cost Price of Stock—` 28,000.]

23. X and Y are partners in a firm. They share profits and losses as X—3/5th and Y—2/5. Their Balance Sheet

as on 1st April, 2018 is given below:

Liabilities ` Assets `

Capital A/cs: Land and Building 3,00,000

X 7,00,000 Plant and Machinery 4,00,000

Y 3,50,000 10,50,000 Patents 1,60,000

Creditors 2,60,000 Stock 2,50,000

Bills Payable 2,40,000 Debtors 3,00,000

Less: Provision for Doubtful Debts 6,000 2,94,000

Cash at Bank 1,46,000

15,50,000 15,50,000

They agree to admit Z into partnership on the following basis:

(a) Z will pay ` 3,00,000 as capital and Capital Accounts of other partners to be adjusted in their new

profit-sharing ratio on the basis of Z’s Capital.

(b) Goodwill of the firm is valued at ` 2,50,000. Z fails to bring his share of goodwill.

(c) Plant and Machinery is to be depreciated by 15%, stock by ` 40,000, Land and Building are to be

appreciated by ` 1,60,000.

(d) New profit-sharing ratio will be 5 : 3 : 2.

Prepare necessary ledger accounts.

[Ans.: Sacrificing Ratio—1 : 1; Revaluation Gain (Profit)—` 60,000; Partners’ Capital A/cs:

X—` 7,50,000; Y—` 4,50,000 and Z—` 3,00,000; Z’s Current A/c—` 50,000; (Dr.);

Cash at Bank—` 4,86,000; Balance Sheet Total—` 20,00,000.]

[Hint: Capitals of old partners are to be adjusted on the basis of incoming partner’s (Z) capital and

Z is unable to bring his share of goodwill of ` 50,000 (i.e., ` 2,50,000 × 2/10), the adjustment for

goodwill will be through his Current A/c. Thus, Z’s Current A/c will be debited by ` 50,000 and

X’s and Y’s Capital A/cs will be credited by ` 25,000 each.]