Page 188 - DEBKVOL-1

P. 188

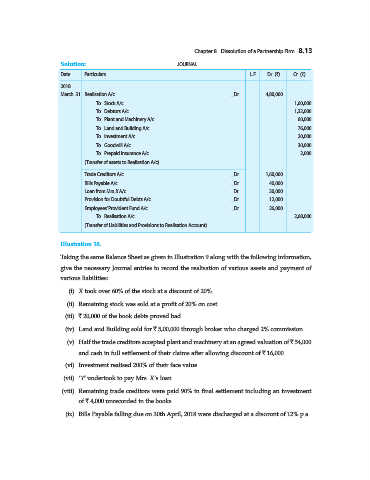

Chapter 8 Dissolution of a Partnership Firm 8.13

.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2018

March 31 Realisation A/c ...Dr. 4,80,000

To Stock A/c 1,60,000

To Debtors A/c 1,32,000

To Plant and Machinery A/c 60,000

To Land and Building A/c 76,000

To Investment A/c 20,000

To Goodwill A/c 30,000

To Prepaid Insurance A/c 2,000

(Transfer of assets to Realisation A/c)

Trade Creditors A/c ...Dr. 1,60,000

Bills Payable A/c ...Dr. 40,000

Loan from Mrs. X A/c ...Dr. 30,000

Provision for Doubtful Debts A/c ...Dr. 12,000

Employees’ Provident Fund A/c ...Dr. 26,000

To Realisation A/c 2,68,000

(Transfer of Liabilities and Provisions to Realisation Account)

Illustration 10.

Taking the same Balance Sheet as given in Illustration 9 along with the following information,

give the necessary Journal entries to record the realisation of various assets and payment of

various liabilities:

(i) X took over 60% of the stock at a discount of 20%.

(ii) Remaining stock was sold at a profit of 20% on cost.

(iii) ` 20,000 of the book debts proved bad.

(iv) Land and Building sold for ` 5,00,000 through broker who charged 2% commission.

(v) Half the trade creditors accepted plant and machinery at an agreed valuation of ` 54,000

and cash in full settlement of their claims after allowing discount of ` 16,000.

(vi) Investment realised 200% of their face value.

(vii) ‘Y’ undertook to pay Mrs. X’s loan.

(viii) Remaining trade creditors were paid 90% in final settlement including an investment

of ` 4,000 unrecorded in the books.

(ix) Bills Payable falling due on 30th April, 2018 were discharged at a discount of 12% p.a.