Page 192 - DEBKVOL-1

P. 192

Chapter 8 Dissolution of a Partnership Firm 8.17

.

The firm was dissolved on 31st March, 2018. The following were the adjustments:

(i) Half of the stock was sold at 10% less than the book value and the remaining half was

taken by Luv at 20% more than the book value.

(ii) During the course of dissolution a liability under action for damages was settled at

` 20,000.

(iii) Assets realised as follows: Plant and Machinery ` 10,00,000, Truck ` 12,00,000. Goodwill

was sold for ` 2,50,000, Bad debts amounted to ` 50,000, half the investments were sold

at book value.

(iv) Luv promised to pay off Mrs. Luv’s Loan and took half the investments at 10% discount.

(v) Trade Creditors and Bills payable were due on average basis of one month after

31st March, but were paid immediately on 31st March at 12% discount per annum.

Prepare Realisation A/c, Partners’ Capital Accounts and Bank Account.

Solution:

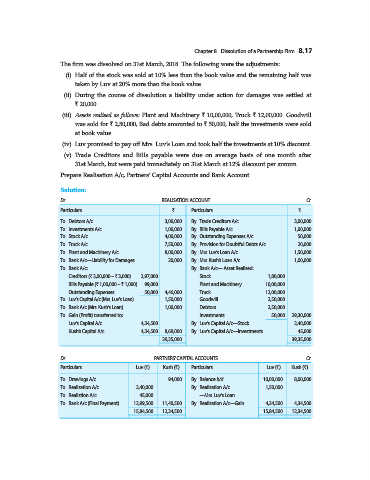

Dr. REALISATION ACCOUNT Cr.

Particulars ` Particulars `

To Debtors A/c 3,00,000 By Trade Creditors A/c 3,00,000

To Investments A/c 1,00,000 By Bills Payable A/c 1,00,000

To Stock A/c 4,00,000 By Outstanding Expenses A/c 50,000

To Truck A/c 7,50,000 By Provision for Doubtful Debts A/c 20,000

To Plant and Machinery A/c 8,00,000 By Mrs. Luv’s Loan A/c 1,50,000

To Bank A/c—Liability for Damages 20,000 By Mrs. Kush’s Loan A/c 1,00,000

To Bank A/c: By Bank A/c— Asset Realised:

Creditors (` 3,00,000 – ` 3,000) 2,97,000 Stock 1,80,000

Bills Payable (` 1,00,000 – ` 1,000) 99,000 Plant and Machinery 10,00,000

Outstanding Expenses 50,000 4,46,000 Truck 12,00,000

To Luv’s Capital A/c (Mrs. Luv’s Loan) 1,50,000 Goodwill 2,50,000

To Bank A/c (Mrs. Kush’s Loan) 1,00,000 Debtors 2,50,000

To Gain (Profit) transferred to: Investments 50,000 29,30,000

Luv’s Capital A/c 4,34,500 By Luv’s Capital A/c—Stock 2,40,000

Kush’s Capital A/c 4,34,500 8,69,000 By Luv’s Capital A/c—Investments 45,000

39,35,000 39,35,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Luv (`) Kush (`) Particulars Luv (`) Kush (`)

To Drawings A/c ... 94,000 By Balance b/d 10,00,000 8,00,000

To Realisation A/c 2,40,000 ... By Realisation A/c 1,50,000 ...

To Realistion A/c 45,000 ... —Mrs. Luv’s Loan

To Bank A/c (Final Payment) 12,99,500 11,40,500 By Realisation A/c—Gain 4,34,500 4,34,500

15,84,500 12,34,500 15,84,500 12,34,500