Page 189 - DEBKVOL-1

P. 189

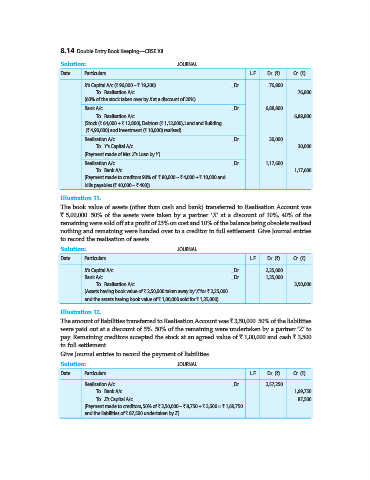

8.14 Double Entry Book Keeping—CBSE XII

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

X‘s Capital A/c (` 96,000 – ` 19,200) ...Dr. 76,800

To Realisation A/c 76,800

(60% of the stock taken over by X at a discount of 20%)

Bank A/c ...Dr. 6,88,800

To Realisation A/c 6,88,800

(Stock (` 64,000 + ` 12,800), Debtors (` 1,12,000), Land and Building

(` 4,90,000) and Investment (` 10,000) realised)

Realisation A/c ...Dr. 30,000

To Y’s Capital A/c 30,000

(Payment made of Mrs. X’s Loan by Y)

Realisation A/c ...Dr. 1,17,600

To Bank A/c 1,17,600

(Payment made to creditors 90% of ` 80,000 – ` 4,000 + ` 10,000 and

bills payables (` 40,000 – ` 400))

Illustration 11.

The book value of assets (other than cash and bank) transferred to Realisation Account was

` 5,00,000. 50% of the assets were taken by a partner ‘X’ at a discount of 10%, 40% of the

remaining were sold off at a profit of 25% on cost and 10% of the balance being obsolete realised

nothing and remaining were handed over to a creditor in full settlement. Give Journal entries

to record the realisation of assets.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

X‘s Capital A/c ...Dr. 2,25,000

Bank A/c ...Dr. 1,25,000

To Realisation A/c 3,50,000

(Assets having book value of ` 2,50,000 taken away by ‘X’ for ` 2,25,000

and the assets having book value of ` 1,00,000 sold for ` 1,25,000)

Illustration 12.

The amount of liabilities transferred to Realisation Account was ` 3,50,000. 50% of the liabilities

were paid out at a discount of 5%. 50% of the remaining were undertaken by a partner ‘Z’ to

pay. Remaining creditors accepted the stock at an agreed value of ` 1,00,000 and cash ` 3,500

in full settlement.

Give Journal entries to record the payment of liabilities.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

Realisation A/c ...Dr. 2,57,250

To Bank A/c 1,69,750

To Z’s Capital A/c 87,500

(Payment made to creditors, 50% of ` 3,50,000 – ` 8,750 + ` 3,500 = ` 1,69,750

and the liabilities of ` 87,500 undertaken by Z)