Page 190 - DEBKVOL-1

P. 190

Chapter 8 Dissolution of a Partnership Firm 8.15

.

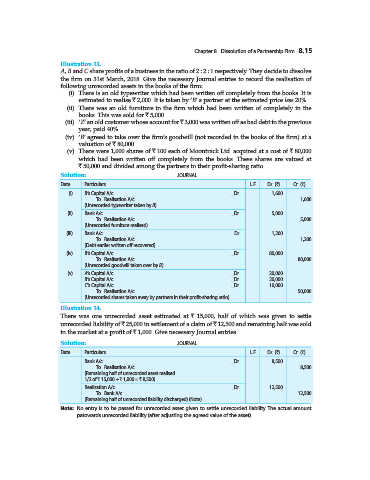

Illustration 13.

A, B and C share profits of a business in the ratio of 2 : 2 : 1 respectively. They decide to dissolve

the firm on 31st March, 2018. Give the necessary Journal entries to record the realisation of

following unrecorded assets in the books of the firm:

(i) There is an old typewriter which had been written off completely from the books. It is

estimated to realise ` 2,000. It is taken by ‘B’ a partner at the estimated price less 20%.

(ii) There was an old furniture in the firm which had been written of completely in the

books. This was sold for ` 5,000.

(iii) ‘Z’ an old customer whose account for ` 3,000 was written off as bad debt in the previous

year, paid 40%.

(iv) ‘B’ agreed to take over the firm’s goodwill (not recorded in the books of the firm) at a

valuation of ` 80,000.

(v) There were 1,000 shares of ` 100 each of Moontrack Ltd. acquired at a cost of ` 80,000

which had been written off completely from the books. These shares are valued at

` 50,000 and divided among the partners in their profit-sharing ratio.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

(i) B‘s Capital A/c ...Dr. 1,600

To Realisation A/c 1,600

(Unrecorded typewriter taken by B)

(ii) Bank A/c ...Dr. 5,000

To Realisation A/c 5,000

(Unrecorded furniture realised)

(iii) Bank A/c ...Dr 1,200

To Realisation A/c 1,200

(Debt earlier written off recovered)

(iv) B‘s Capital A/c ...Dr. 80,000

To Realisation A/c 80,000

(Unrecorded goodwill taken over by B)

(v) A’s Capital A/c ...Dr. 20,000

B’s Capital A/c ...Dr. 20,000

C’s Capital A/c ...Dr. 10,000

To Realisation A/c 50,000

(Unrecorded shares taken away by partners in their profit-sharing ratio)

Illustration 14.

There was one unrecorded asset estimated at ` 15,000, half of which was given to settle

unrecorded liability of ` 25,000 in settlement of a claim of ` 12,500 and remaining half was sold

in the market at a profit of ` 1,000. Give necessary Journal entries.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

Bank A/c ...Dr. 8,500

To Realisation A/c 8,500

(Remaining half of unrecorded asset realised

1/2 of ` 15,000 + ` 1,000 = ` 8,500)

Realisation A/c ...Dr. 12,500

To Bank A/c 12,500

(Remaining half of unrecorded liability discharged) (Note)

Note: No entry is to be passed for unrecorded asset given to settle unrecorded liability. The actual amount

patowards unrecorded liability (after adjusting the agreed value of the asset).