Page 46 - DEBKVOL-1

P. 46

2.18 Double Entry Book Keeping—CBSE XII

Solution:

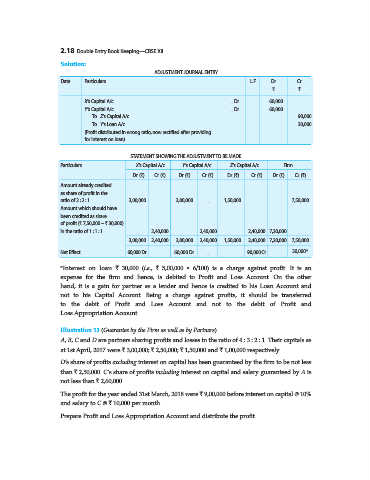

ADJUSTMENT JOURNAL ENTRY

Date Particulars L.F. Dr. Cr.

` `

X’s Capital A/c ...Dr. 60,000

Y’s Capital A/c ...Dr. 60,000

To Z’s Capital A/c 90,000

To Y’s Loan A/c 30,000

(Profit distributed in wrong ratio, now rectified after providing

for interest on loan)

STATEMENT SHOWING THE ADJUSTMENT TO BE MADE

Particulars X’s Capital A/c Y’s Capital A/c Z’s Capital A/c Firm

Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`)

Amount already credited

as share of profit in the

ratio of 2 : 2 : 1 3,00,000 ... 3,00,000 ... 1,50,000 ... ... 7,50,000

Amount which should have

been credited as share

of profit (` 7,50,000 – ` 30,000)

in the ratio of 1 : 1 : 1 ... 2,40,000 ... 2,40,000 ... 2,40,000 7,20,000 ...

3,00,000 2,40,000 3,00,000 2,40,000 1,50,000 2,40,000 7,20,000 7,50,000

Net Effect 60,000 Dr. ... 60,000 Dr. ... ... 90,000 Cr. ... 30,000*

*Interest on loan ` 30,000 (i.e., ` 5,00,000 × 6/100) is a charge against profit. It is an

expense for the firm and hence, is debited to Profit and Loss Account. On the other

hand, it is a gain for partner as a lender and hence is credited to his Loan Account and

not to his Capital Account. Being a charge against profits, it should be transferred

to the debit of Profit and Loss Account and not to the debit of Profit and

Loss Appropriation Account.

Illustration 13 (Guarantee by the Firm as well as by Partners).

A, B, C and D are partners sharing profits and losses in the ratio of 4 : 3 : 2 : 1. Their capitals as

at 1st April, 2017 were ` 3,00,000; ` 2,50,000; ` 1,50,000 and ` 1,00,000 respectively.

D’s share of profits excluding interest on capital has been guaranteed by the firm to be not less

than ` 2,50,000. C’s share of profits including interest on capital and salary guaranteed by A is

not less than ` 2,60,000.

The profit for the year ended 31st March, 2018 were ` 9,00,000 before interest on capital @ 10%

and salary to C @ ` 10,000 per month.

Prepare Profit and Loss Appropriation Account and distribute the profit.